Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

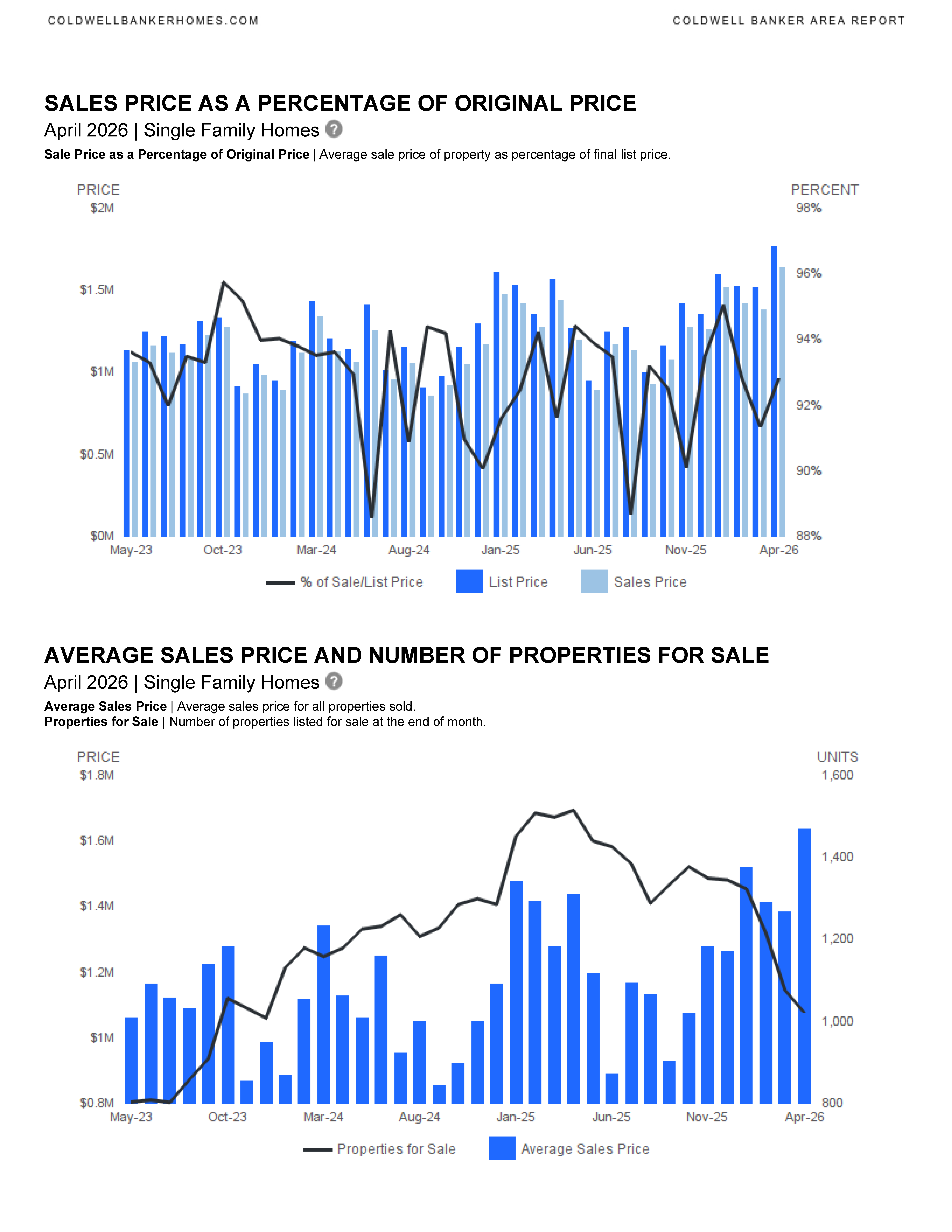

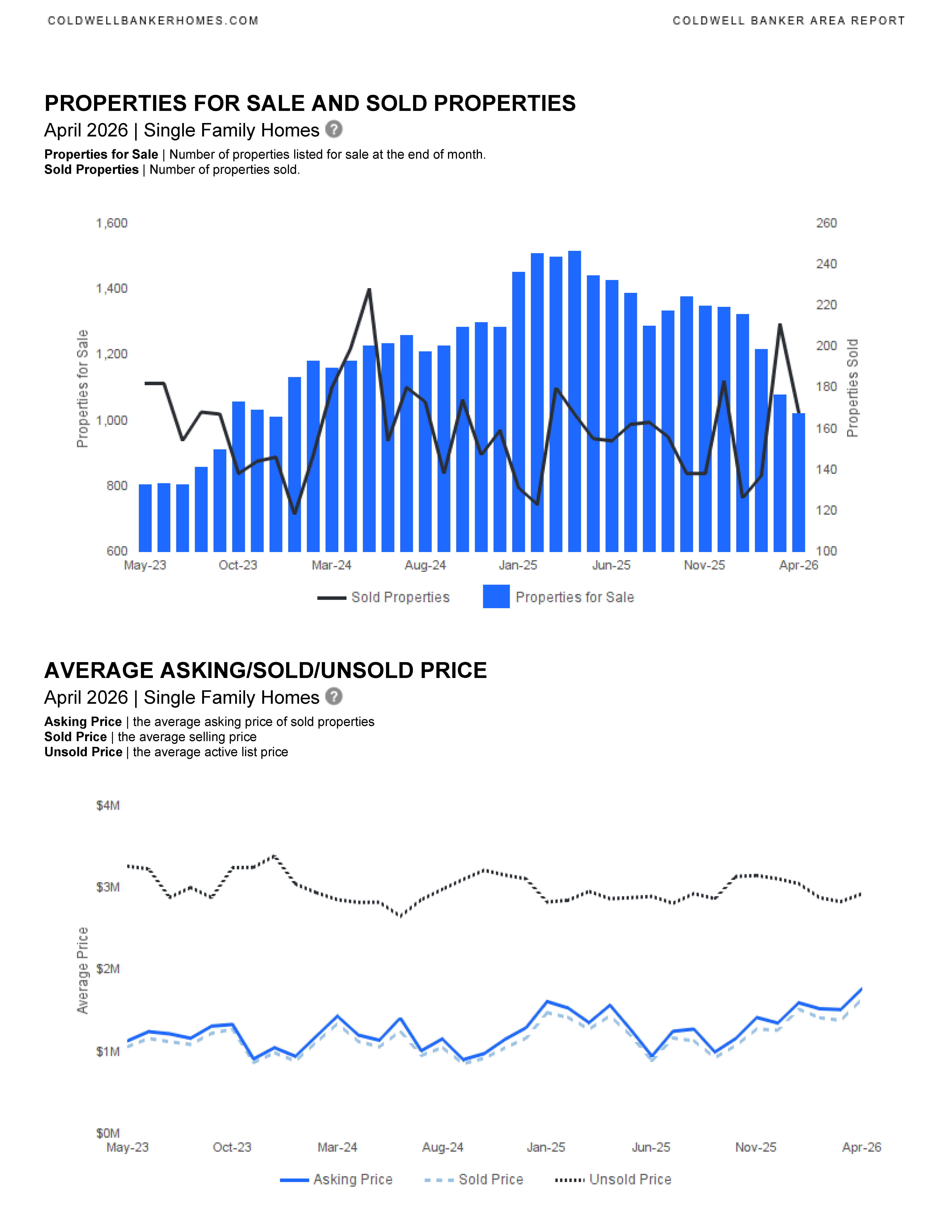

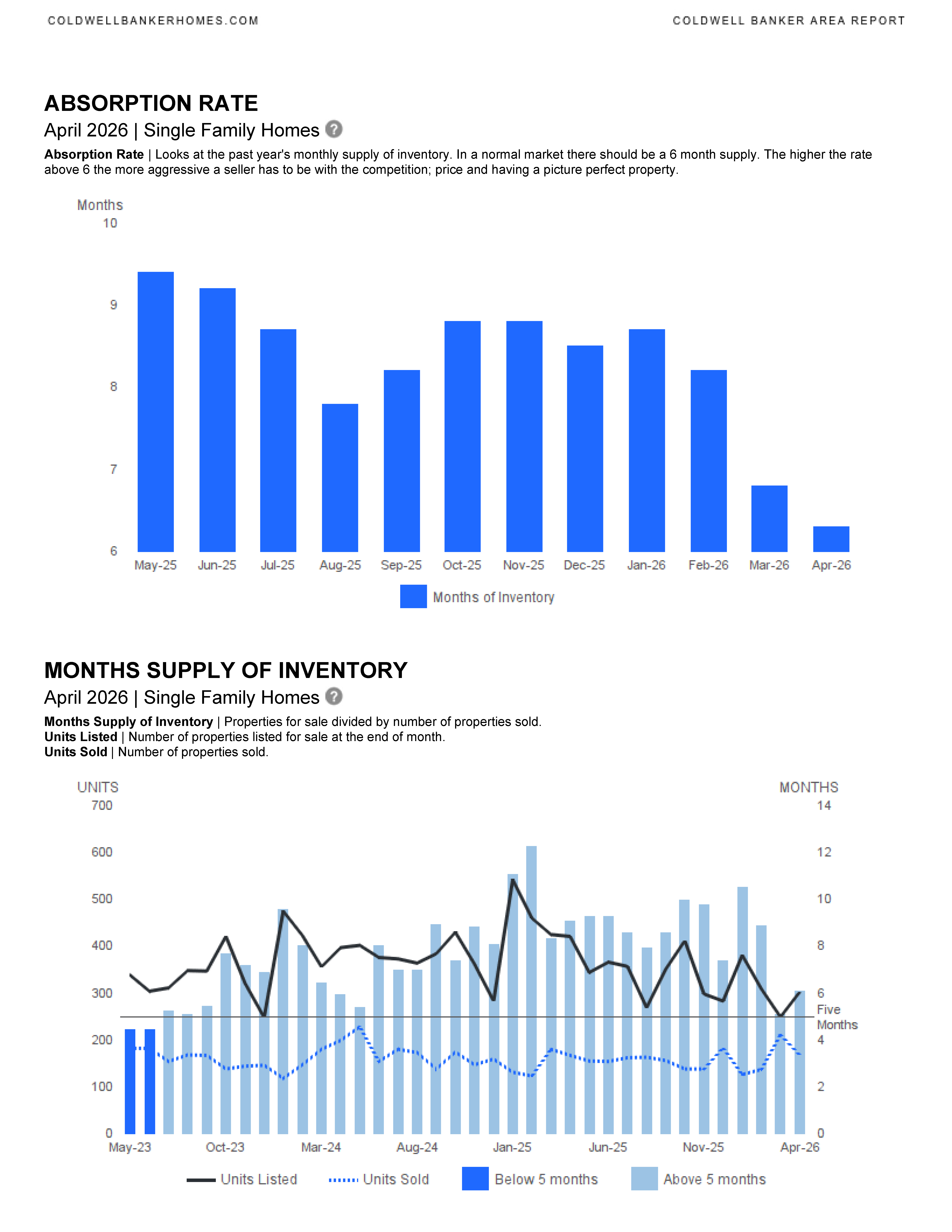

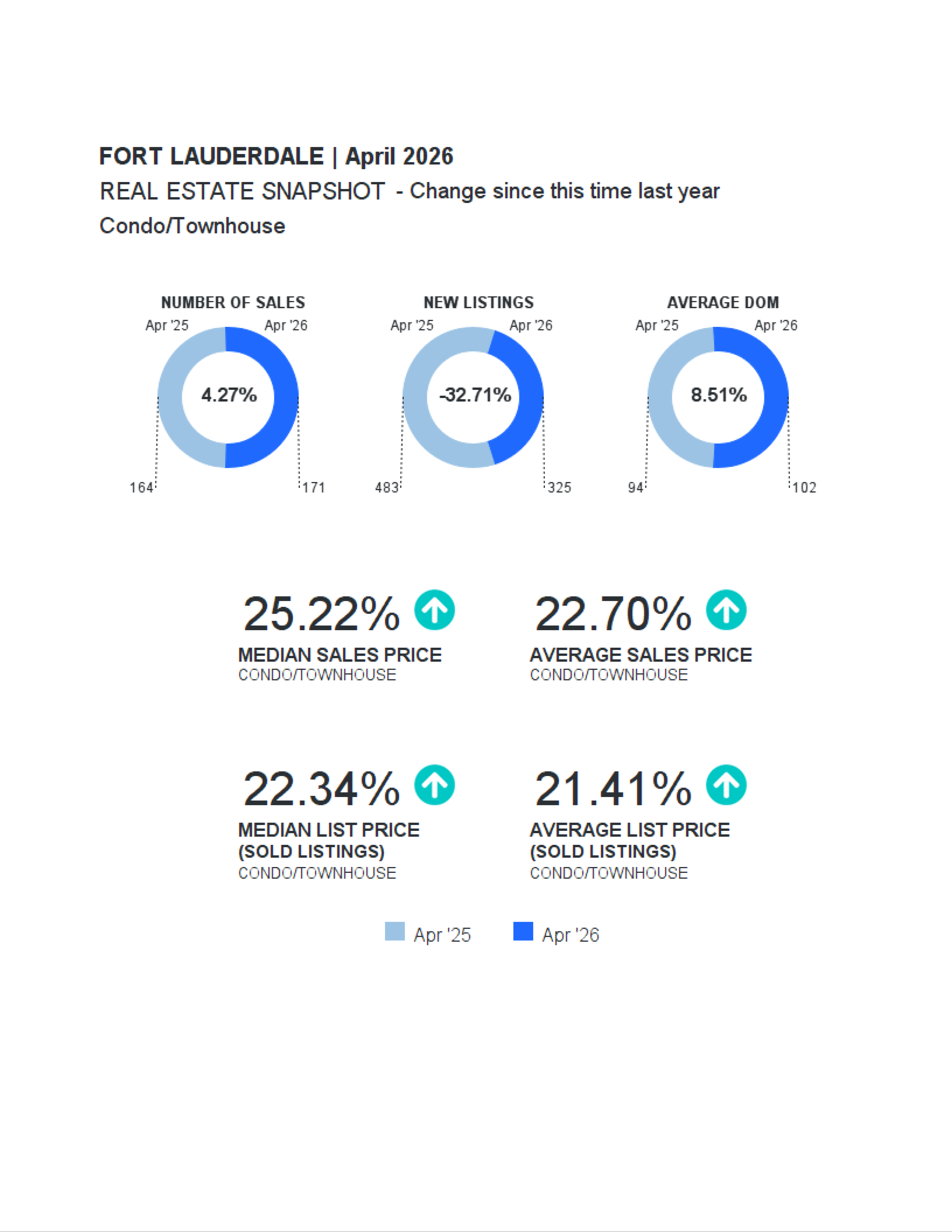

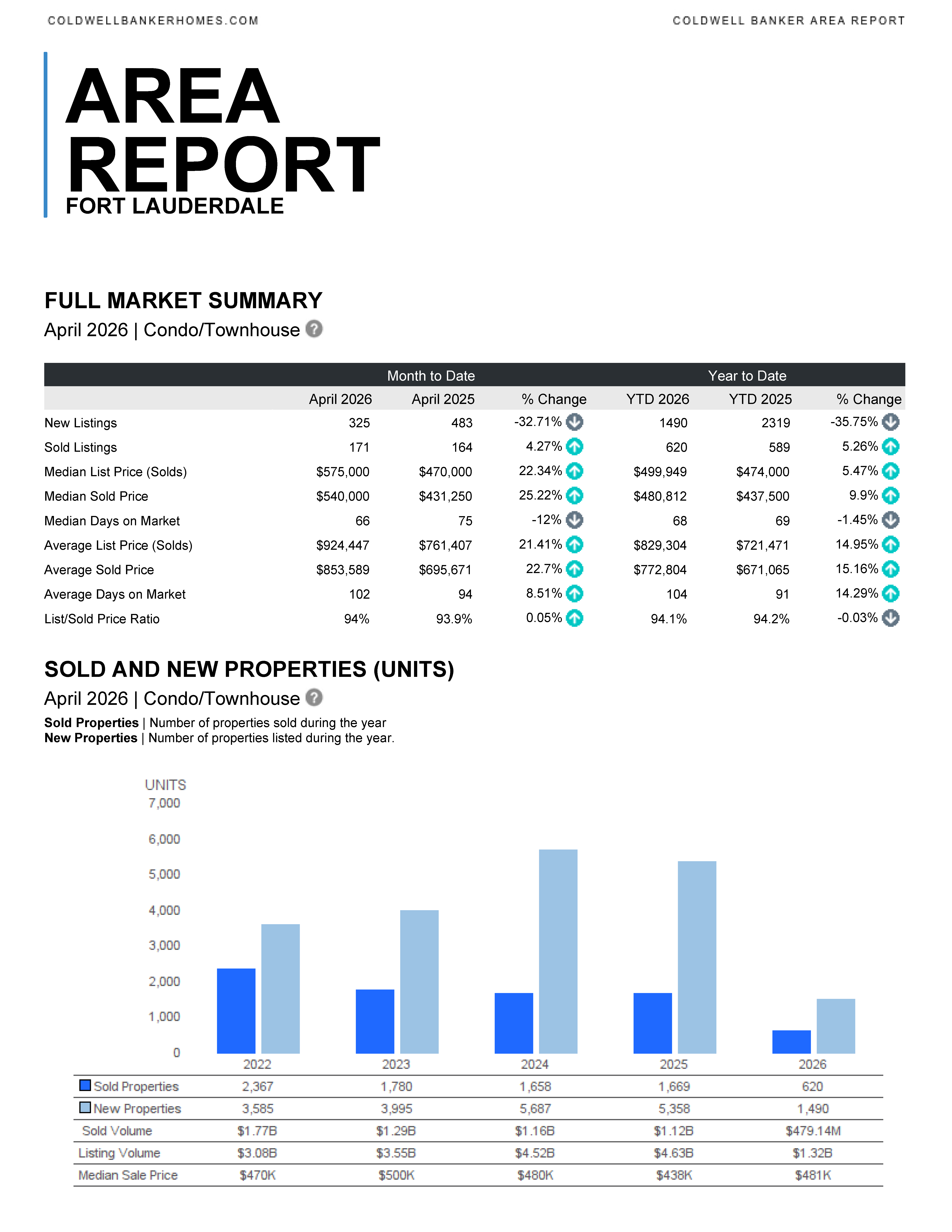

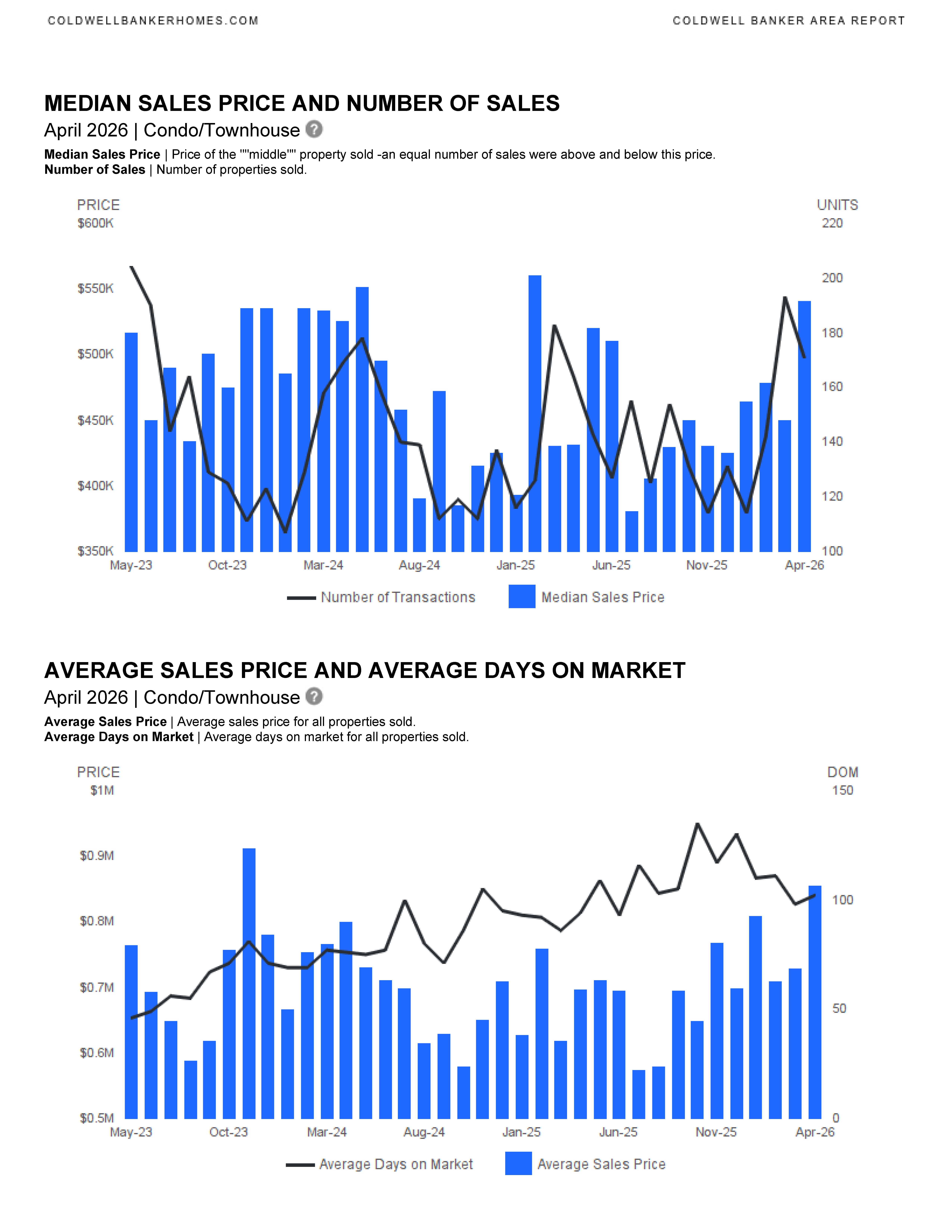

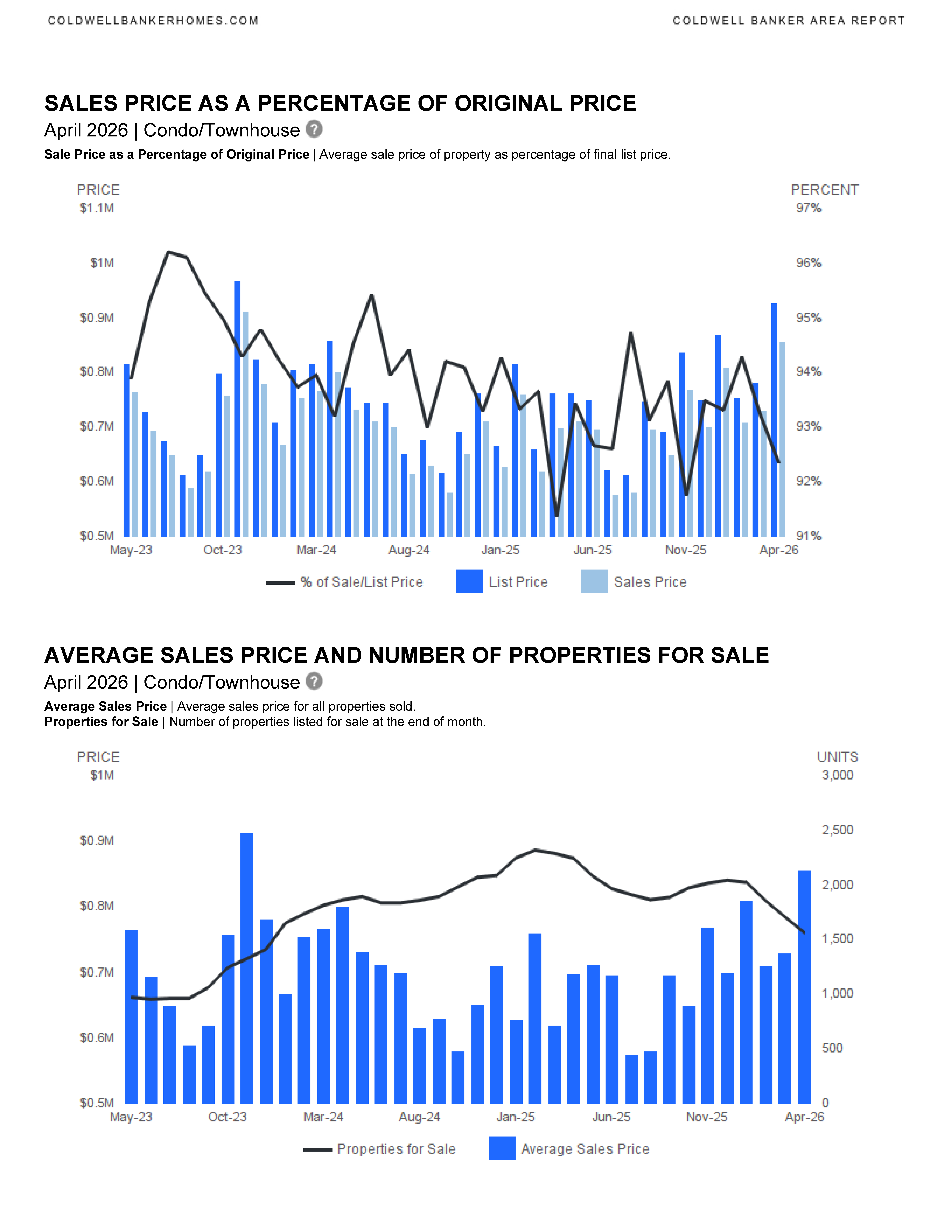

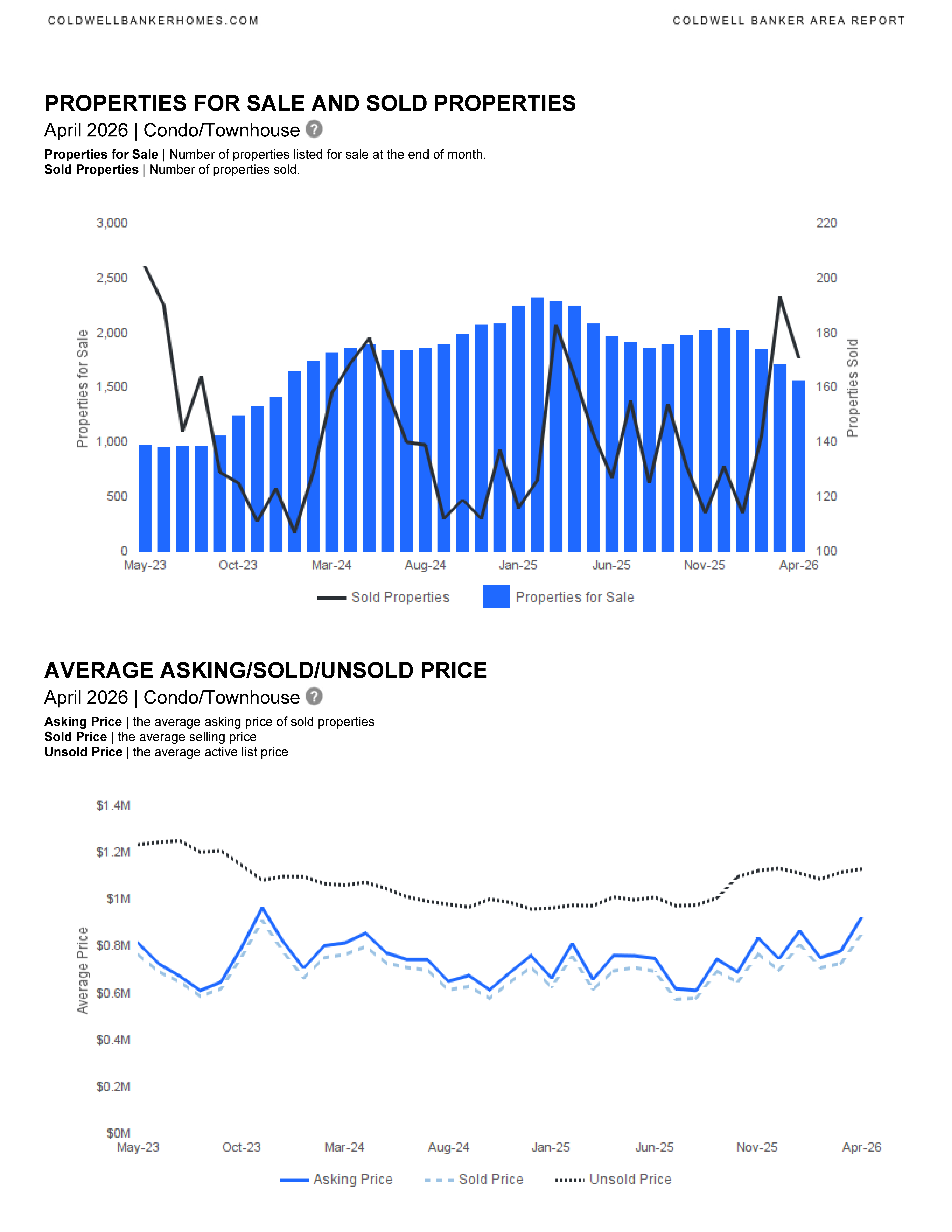

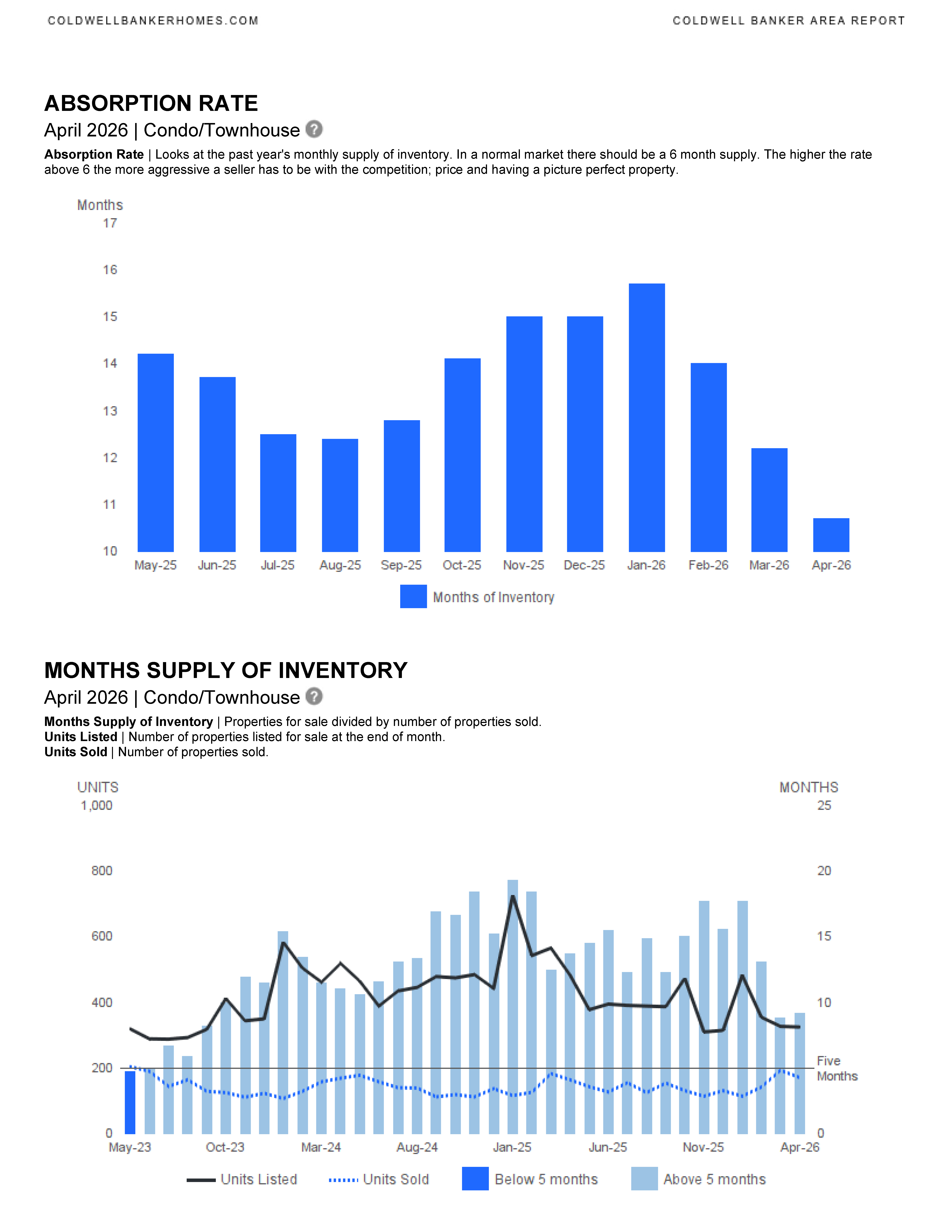

Fort Lauderdale April 2026 Area Report

Fort Lauderdale April 2026 real estate statistics have been published.

Single Family Homes

Condominium & Townhouses

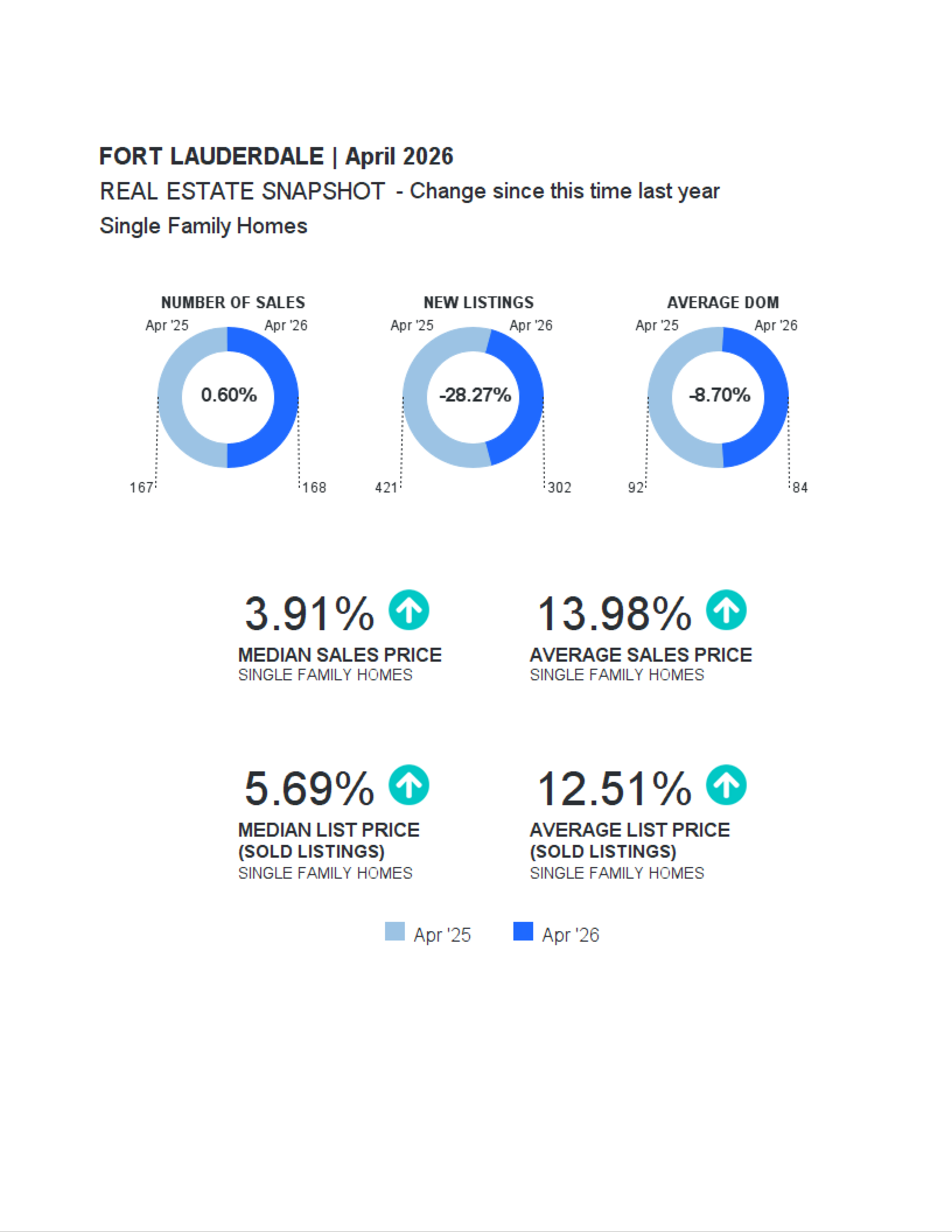

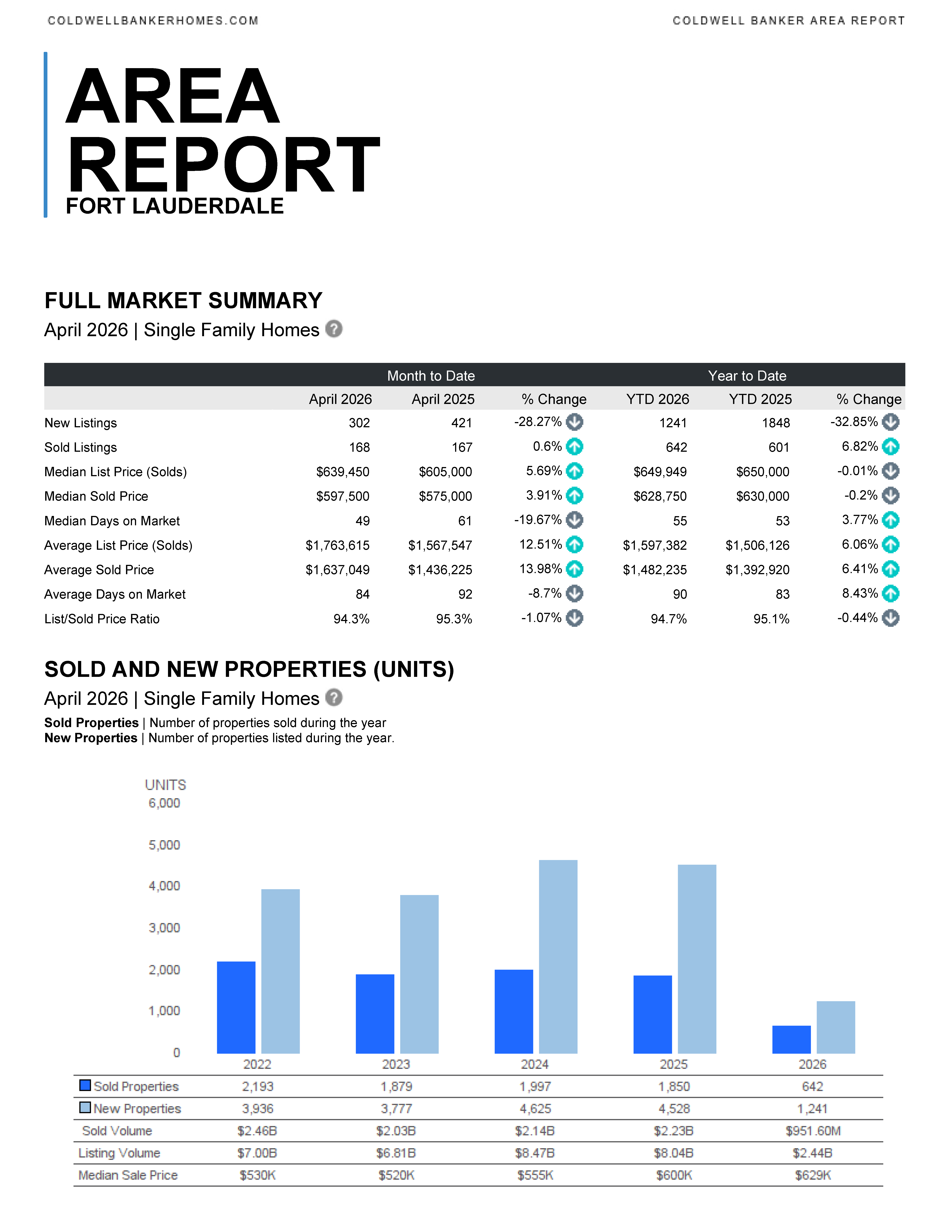

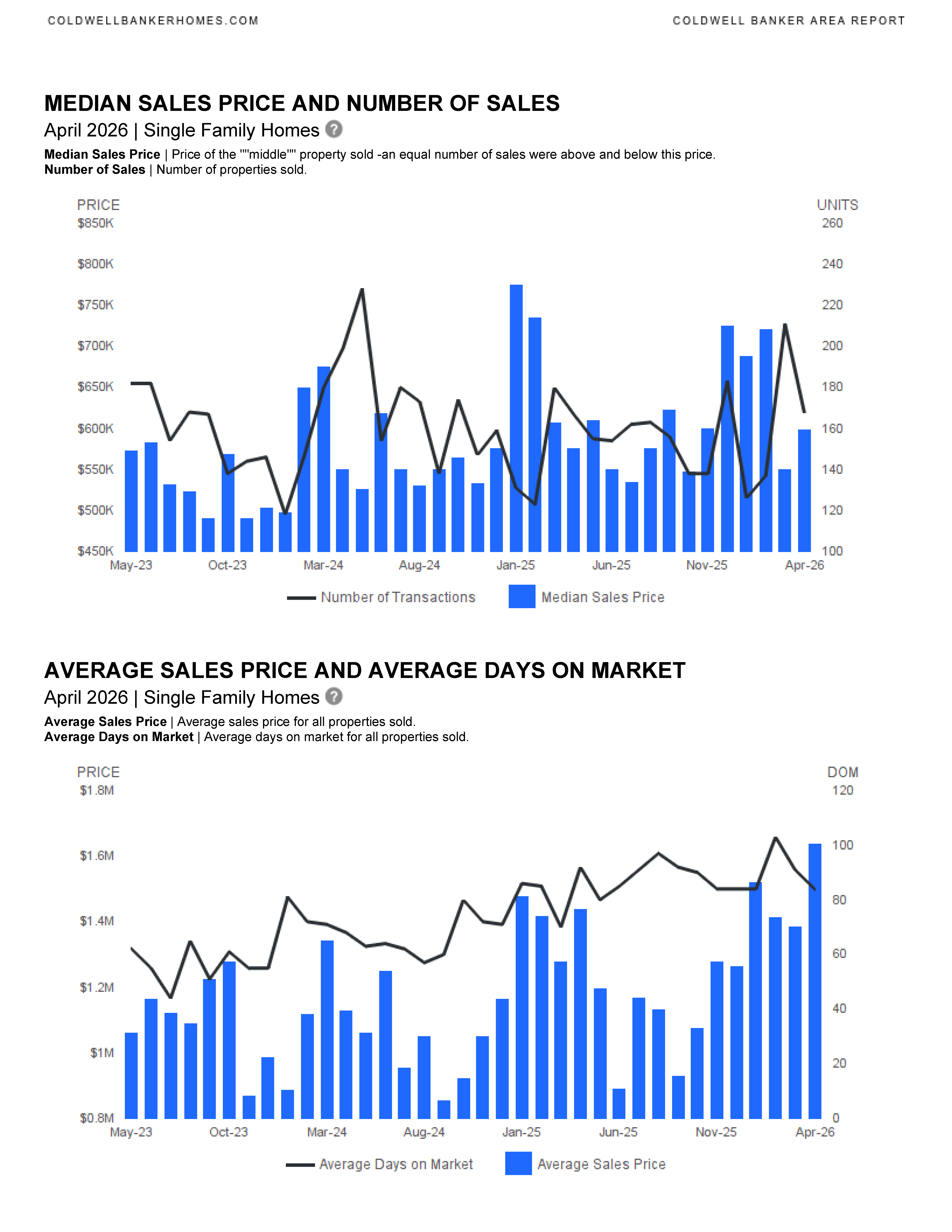

🏡 Single-Family Homes – Key Highlights

- Prices are rising steadily

- Median sold price: ↑ 3.9% ($597,500)

- Average sold price: ↑ 14.0%

- Inventory is tightening

- New listings: ↓ 28.3% year-over-year

- Sales are holding steady

- Homes sold: ↑ 0.6% (essentially flat)

- Homes are selling faster

- Median days on market: 49 days (↓ ~20%)

- Average days on market: ↓ 8.7%

- Slight negotiation returning

- Sale-to-list price ratio dipped to ~94.3%

🏙️ Condo & Townhouse Market – Key Highlights

- Prices are surging

- Median sold price: ↑ 25.2% ($540,000)

- Average sold price: ↑ 22.7%

- Inventory dropped significantly

- New listings: ↓ 32.7%

- More sales activity

- Homes sold: ↑ 4.3%

- Mixed timing trends

- Median days on market: ↓ 12% (faster)

- Average days on market: ↑ 8.5% (some properties linger)

- Pricing remains strong

- Sale-to-list ratio: ~94% (stable)

📦 Inventory & Supply Trends (Overall Insight)

- Inventory is decreasing across both property types (fewer new listings year-over-year)

- Months of supply is trending near or just above balanced levels (around the 6-month benchmark, per report visuals)

- Sellers are facing more competition than peak frenzy years, but still benefiting from strong pricing

✅ Major Takeaways

- 📈 Prices are rising across the board, especially in the condo market

- 📉 Inventory shortages continue, limiting buyer options

- ⚖️ Sales activity is stable, not surging

- ⏱️ Homes are generally selling faster, especially well-priced ones

- 💬 Negotiation is slightly increasing, but sellers still hold leverage

🧭 Bottom Line: What Kind of Market Is It?

Fort Lauderdale remains a strong but stabilizing seller’s market.

- Sellers: Still have pricing power, but need to be competitive as buyers become more selective

- Buyers: Facing limited inventory and higher prices, but beginning to gain slightly more negotiating room

In today’s competitive SE Florida housing market, it’s essential to work with an experienced and knowledgeable real estate professional. If you’d like up‑to‑date market reports for your neighborhood, Fort Lauderdale, or any other SE Florida community, I’d be happy to send them. We can review current trends, discuss the market, and explore how we can work together to achieve your real estate goals. I’m here to support you every step of the way.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

SE Florida Market Snapshot – April 2026

Market Trends in SE Florida

Snapshot of today’s Broward County market

- Prices: Median listing prices are roughly flat to slightly down year‑over‑year. Keep in mind there are “markets within markets”.

- Inventory: Active listings are high and have grown over the last few years, giving buyers more choices and easing bidding wars.

- Days on market: Homes are taking longer to sell (around 80–90 days on average), which signals a cooler, more negotiable market than the frenzy of a few years ago.

- Segment split: Single‑family homes are holding value better, while condos/townhomes have softened more due to stricter regulations, insurance costs, and higher rates.

Overall, Broward is in a balanced-to-cool phase: still active, but with more leverage and time for buyers, and a need for sharper strategy from sellers.

Advice for buyers

- Leverage the extra inventory, but don’t overplay your hand

- You often have multiple options and more time to decide—use that to compare HOA fees, insurance quotes, and reserves (especially for condos).

- Focus on total monthly cost, not just price

- Insurance + taxes + HOA can swing affordability more than a small price difference, particularly in Broward’s coastal and condo markets. Get quotes early and build them into your budget.

- Negotiate with data

- Use recent days‑on‑market and price reductions in the neighborhood to justify your offer and repair credits. In a cooler market, sellers are more open to concessions on closing costs, repairs, or rate buydowns.

- Be picky about building quality and reserves

- For condos, review the budget, reserves, and recent engineering reports. Newer safety and reserve rules can mean higher assessments—better to know now than be surprised later.

- Get pre‑approved and be clear on your walk‑away line

- A strong, clean pre‑approval still stands out. Decide in advance the max payment you’re comfortable with so you don’t stretch just because a property feels “perfect.”

Advice for sellers

- Price for today’s market, not yesterday’s peak

- With prices slightly correcting and days on market rising, overpricing is the fastest way to sit stale and invite lowball offers. Start at a realistic, data‑backed price that matches recent closed sales, not just active listings.

- Win on presentation

- In a higher‑inventory market, your home is competing hard for attention. Professional photos, good lighting, decluttering, minor repairs, and neutral paint can be the difference between “scroll past” and “schedule a showing.”

- Be ready to negotiate—and to give value

- Buyers now expect something: a price adjustment, closing cost help, or a credit for updates. Decide ahead of time what you’re willing to offer so you can respond quickly and keep good buyers engaged.

- Mind the first 2–3 weeks on market

- That’s when you get the most eyeballs. If showings are slow or feedback is consistently about price, adjust quickly rather than waiting months and chasing the market down.

- For condo sellers: get your paperwork tight

- Have association docs, budgets, reserves, and recent inspections ready. The smoother and more transparent the building looks, the less nervous buyers (and their lenders) will be.

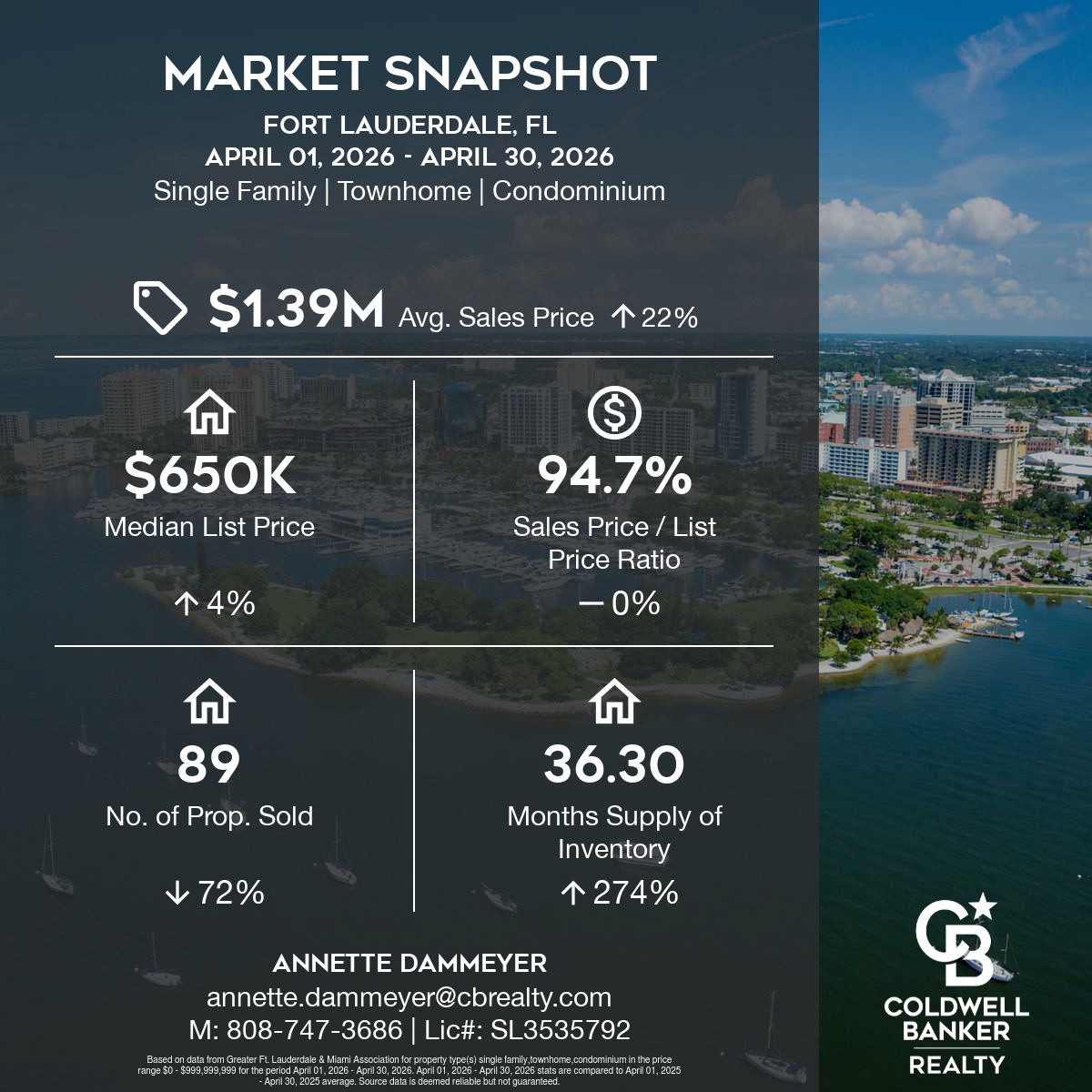

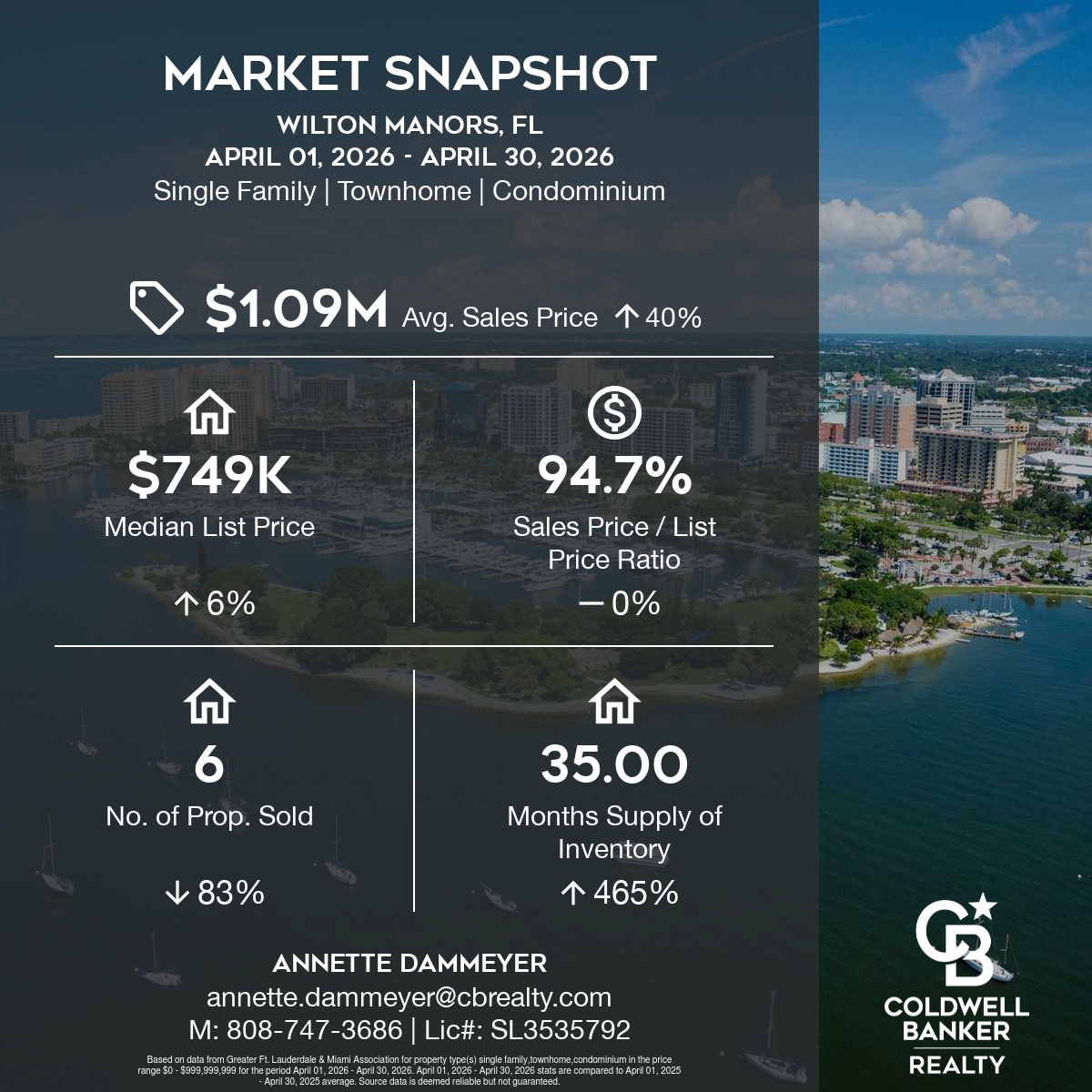

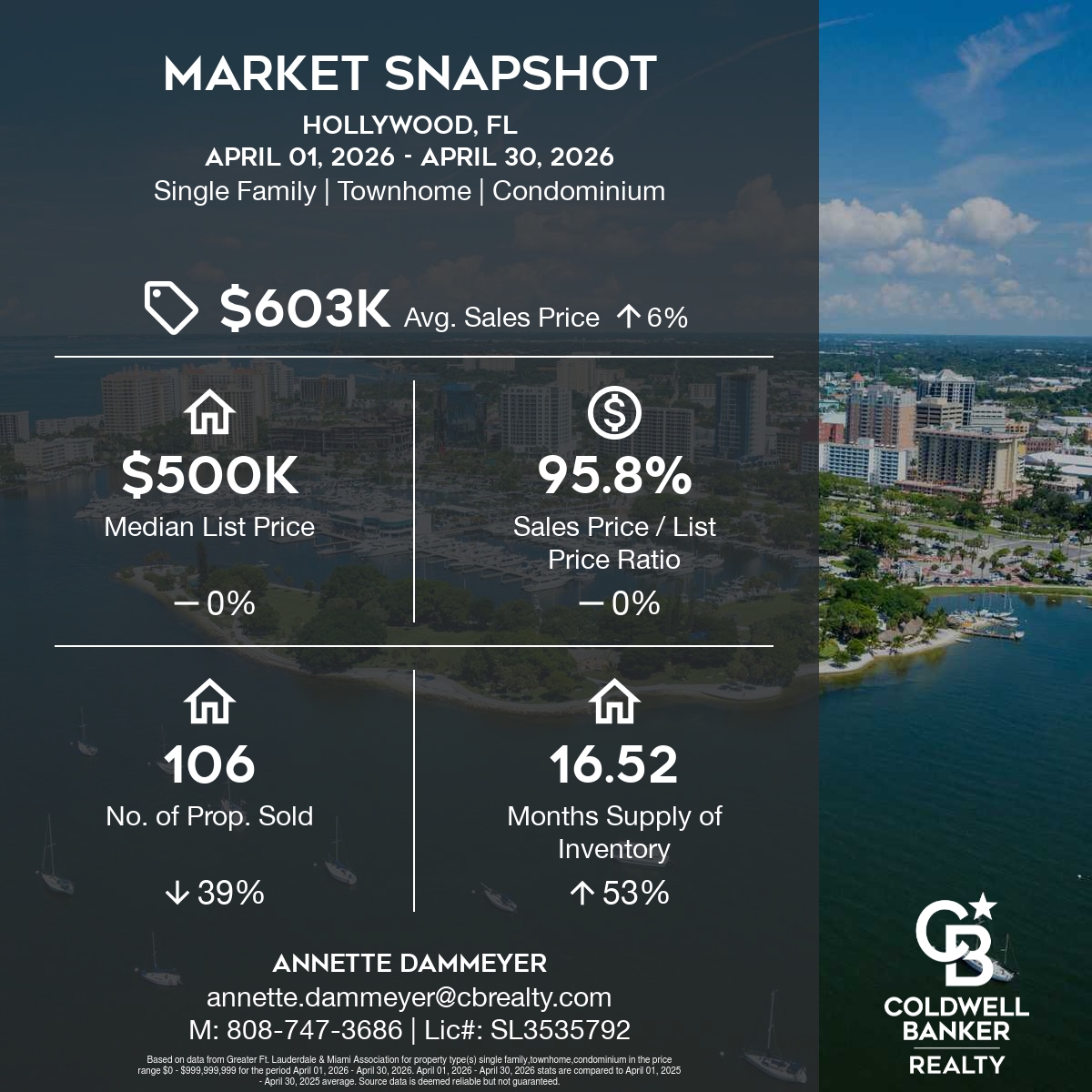

Here are the Market Snapshots reflecting the last month (compared to the same month last year) for the following areas:

- Fort Lauderdale

- Wilton Manors

- Hollywood

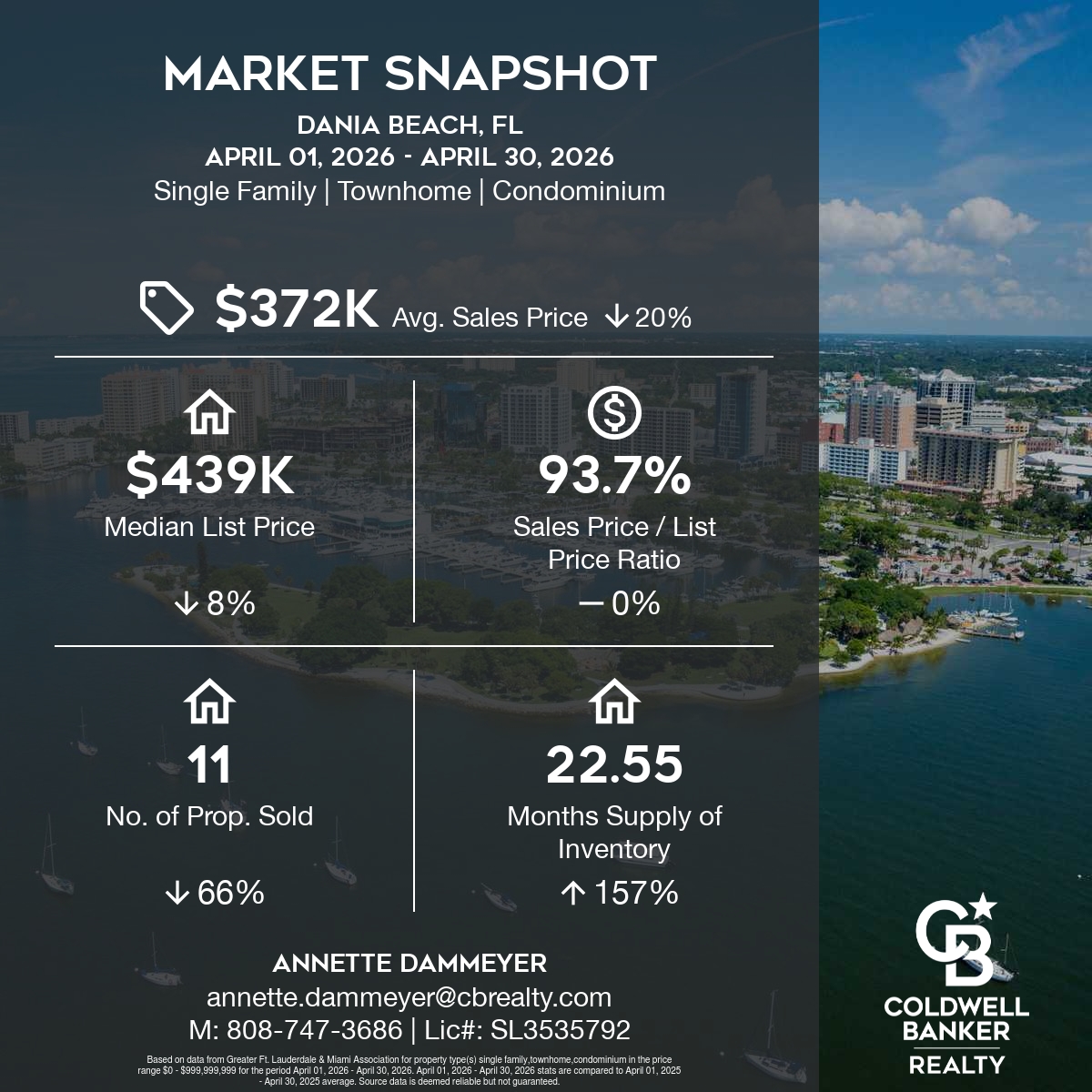

- Dania Beach

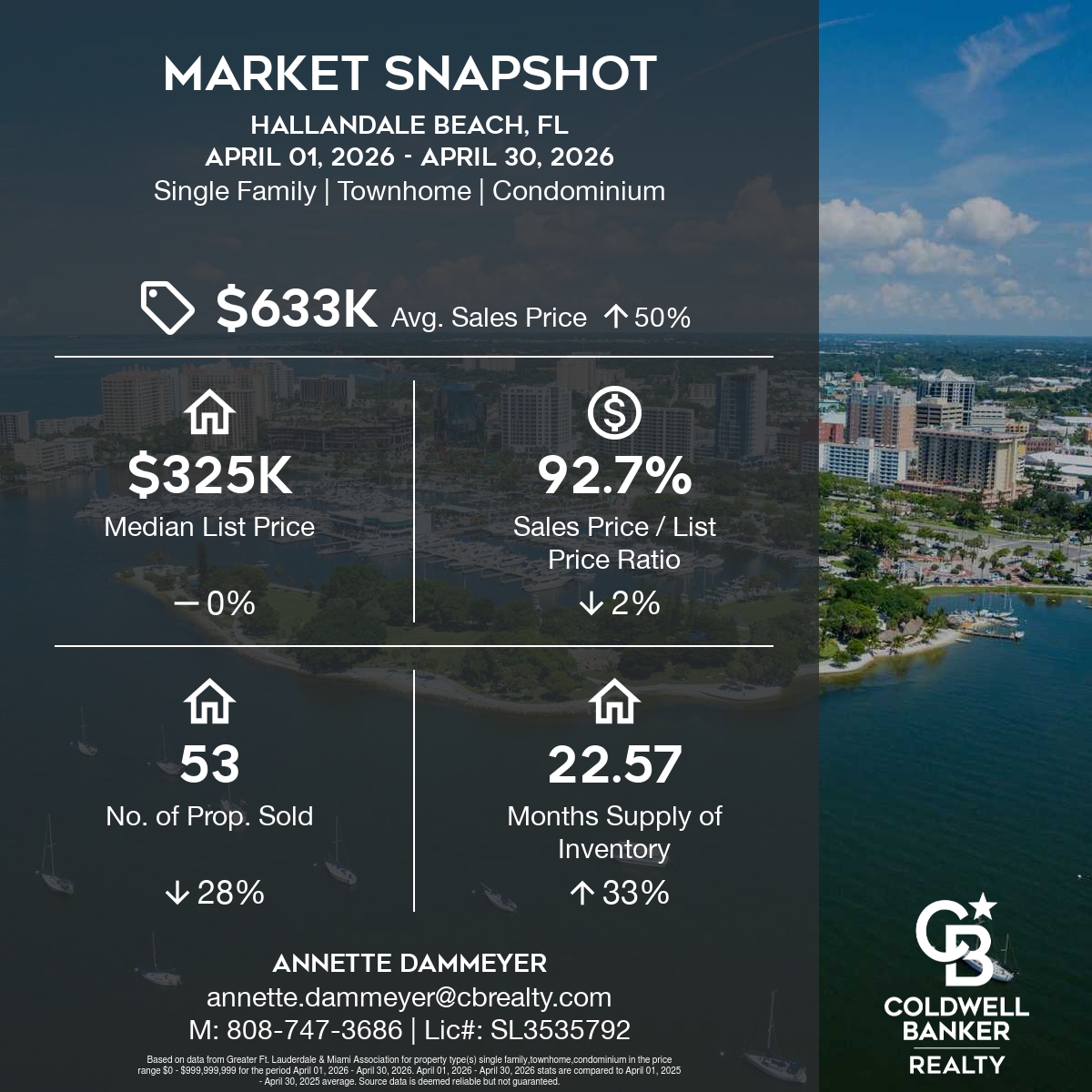

- Hallandale Beach

These take into account all property types (Single Family Homes/Condos/Townhomes).

The real estate landscape in South Florida is evolving. Making smart, timely decisions has never been more important. Whether you’re considering selling, buying, or simply staying informed, I’m here to be your local advisor and resource.

Let’s talk about current market trends and how we can align your goals with today’s opportunities. I’d be happy to provide customized market reports for Fort Lauderdale, any SE Florida city, or even your specific neighborhood—all automatically delivered to your inbox.

Call or email me anytime. I’m here to help you move forward with clarity and confidence.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

May 2026 ~ Seller Safety, Top Home Tech and Summer Enjoyment

May 2026 NewsletterWelcome to Your May 2026 Real Estate & Lifestyle Update!

Welcome to May in Southeast Florida, a season when our homes become hubs for entertaining, innovation, and fresh starts. As a local real estate professional who has guided buyers and sellers through every kind of market, my top priority has always been keeping our community informed, empowered, and protected—both inside and outside the home. In this month’s newsletter, I’m sharing timely insights every Southeast Florida homeowner and seller should know. We’ll begin with seller safety during home showings, including smart, proactive steps to help protect your home, valuables, and peace of mind in today’s fast-moving market. You’ll also discover the best home gadgets transforming daily living in 2026, from stair climbing robot vacuums to convenience-driven tech that today’s buyers are actively seeking. With summer right around the corner, we’ll explore outdoor entertaining trends that are redefining how we live and gather—think relaxed lounge zones, layered ambiance, and seasonal styling designed for our Southeast Florida lifestyle. We’ll also take a closer look at walkability, why it continues to impact home values and quality of life, and which neighborhood features matter most as buyers think beyond the home itself. As always, I’ve also included the latest area reports so you can stay informed on how our local markets are performing across Southeast Florida. Together, these topics reflect how real estate, lifestyle, and smart planning intersect—especially here at home. Let’s dive in. |

|||||||||||

|

National Stories

|

|||||||||||

|

|

|||||||||||

Real Estate Updates | Area Reports | March 2026

|

⇒ CONTACT ANNETTE ⇐

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

![]()

Seller Safety During Home Showings

🏡 When Your Home Is on the Market, Safety Comes First

A veteran real estate agent’s guide to protecting your home, valuables, and family during showings

As an experienced real estate agent who has guided hundreds of families through buying and selling homes, my priority goes beyond closing deals—I care deeply about keeping our community safe, informed, and protected.

When a home is listed, it naturally attracts more foot traffic. Most visitors are genuine buyers and professionals—but increased access means increased responsibility. Here’s how to stay vigilant without adding stress.

(Get your FREE printable checklist below ⇓⇓⇓⇓)

🚪 Why Home Safety Matters During Showings

Selling a home can mean many different types of visitors, including:

- 🧑🤝🧑 Private buyers at open houses

- 👨👩👧 Families touring during scheduled showings

- 🧑🔧 Inspectors, appraisers, photographers

- 🧼 Cleaners, stagers, contractors

Each visit is legitimate—but the volume and variety mean it’s important to assume nothing and prepare for everything.

🔐 How to Protect High-Value & Sensitive Items

💎 Jewelry & Small Valuables

- Store in a locked safe or remove from the home entirely

- Never leave jewelry in bathroom drawers or on nightstands

- Don’t assume “out of sight” is out of risk

📄 Confidential Documents

Protect anything with your:

- Social Security number

- Bank or mortgage info

- Medical or insurance records

✅ Action:

Scan what you need and store originals in a locking file cabinet or offsite.

💊 Prescriptions & Medications

- Secure medications in locked cabinets

- Especially important for controlled substances

- Prevent theft, misuse, or accidental access by children

🔫 Firearms

- Firearms should always be:

- Unloaded

- Stored in a locked safe

- With ammunition locked separately

This protects visitors, your family, and you from serious liability.

🍷 Expensive or Collectible Wine

- Wine collections are often overlooked

- Secure rare or high-value bottles in locked storage

- Consider temporarily relocating investment-grade wine

👀 Stay Vigilant During Showings

- ✅ Use scheduled showings only—avoid surprise visits

- ✅ Work with agents who verify buyers before tours

- ✅ Install smart locks or security systems

- ✅ Keep a log of showings and visitors

💡 Pro tip: discreet entryway cameras (where legal) can add peace of mind.

👨👩👧 Personal Safety for You & Your Family

Your home should feel like a sanctuary—even during a sale.

Practical steps:

- Avoid being home alone during showings

- Step out for open houses when possible

- Let a trusted neighbor know when your home is being shown

- Keep phones charged and accessible

- Trust your instincts—if something feels off, speak up

✅ Key Takeaways

✔ Increased traffic = increased responsibility

✔ Lock, store, or remove valuables and documents

✔ Protect medications, firearms, and specialty items

✔ Prioritize personal safety, not just property

✔ A good agent protects you, not just your listing

⇒ FREE PRINTABLE CHECKLIST ⇐

Selling your home should be exciting—not stressful. With smart preparation and vigilance, you can protect what matters most while welcoming the right buyers with confidence.

If you ever have questions about safe showing practices, I’m here. Our community’s safety always comes first. 💙

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

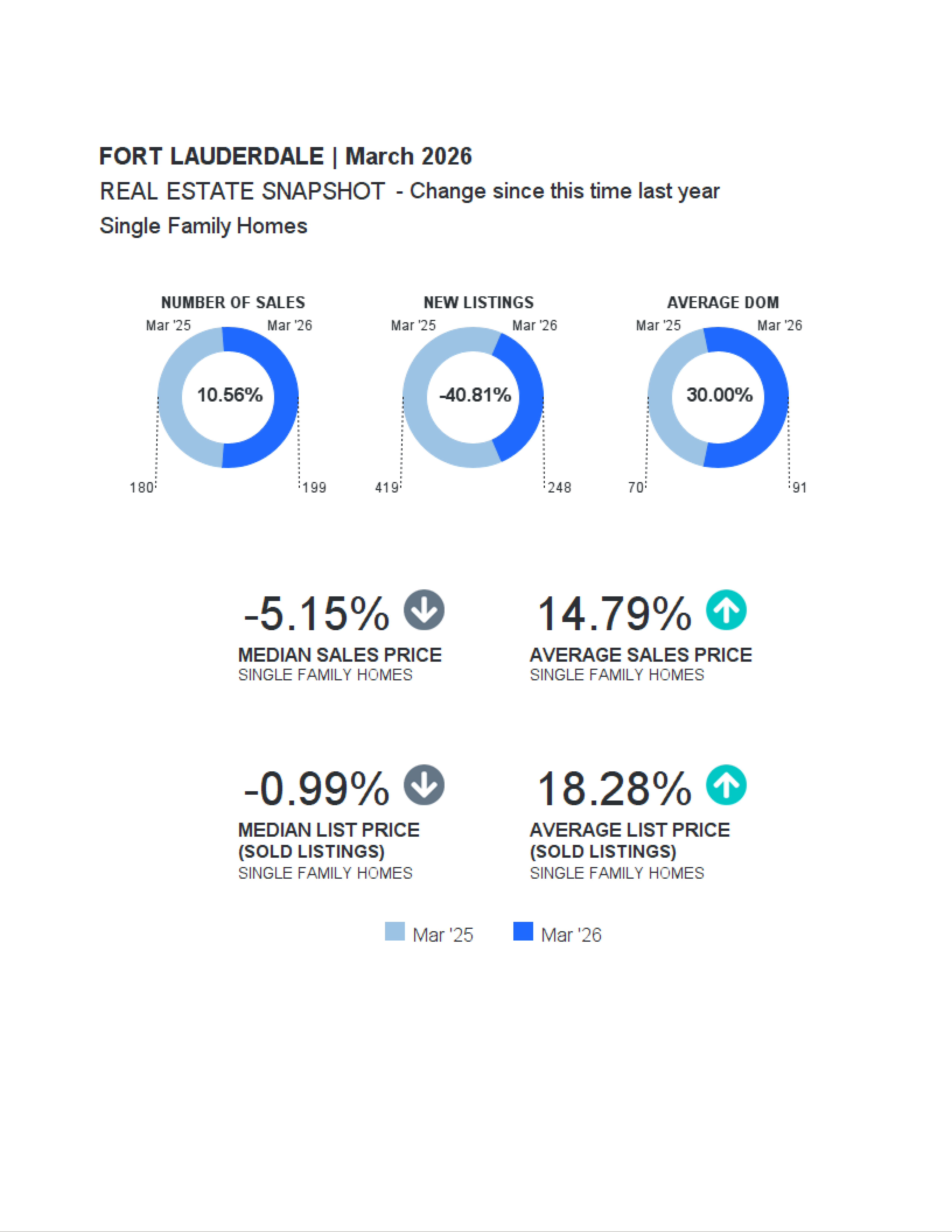

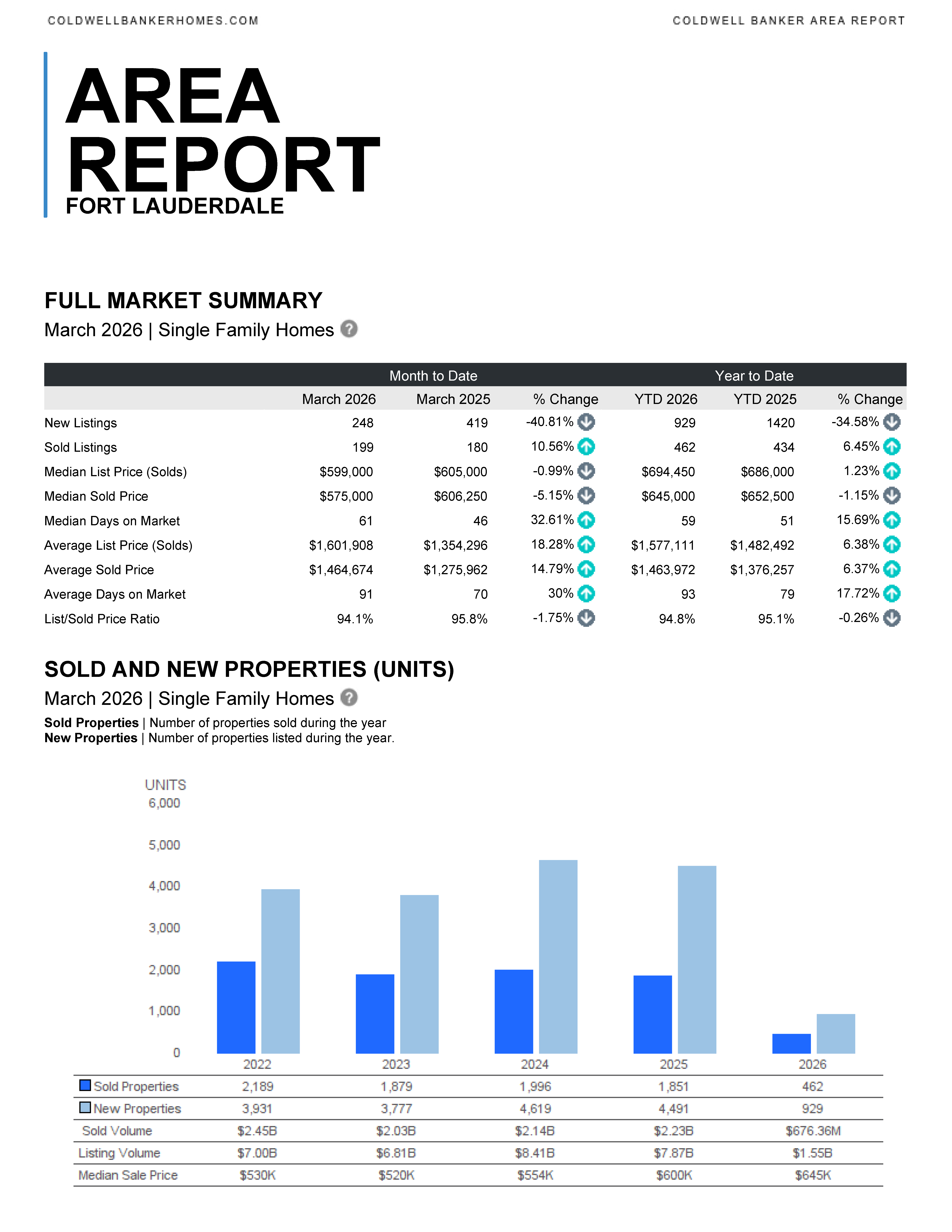

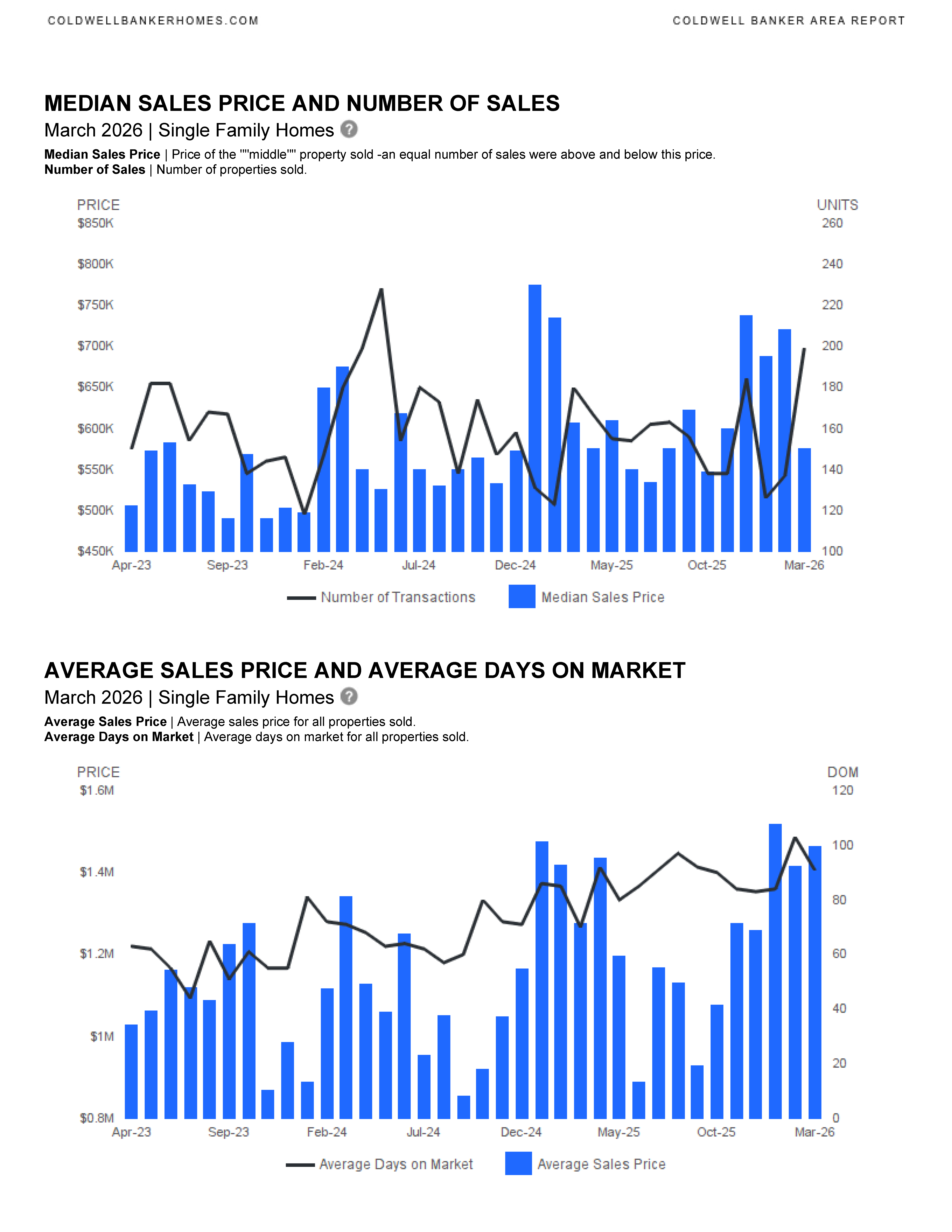

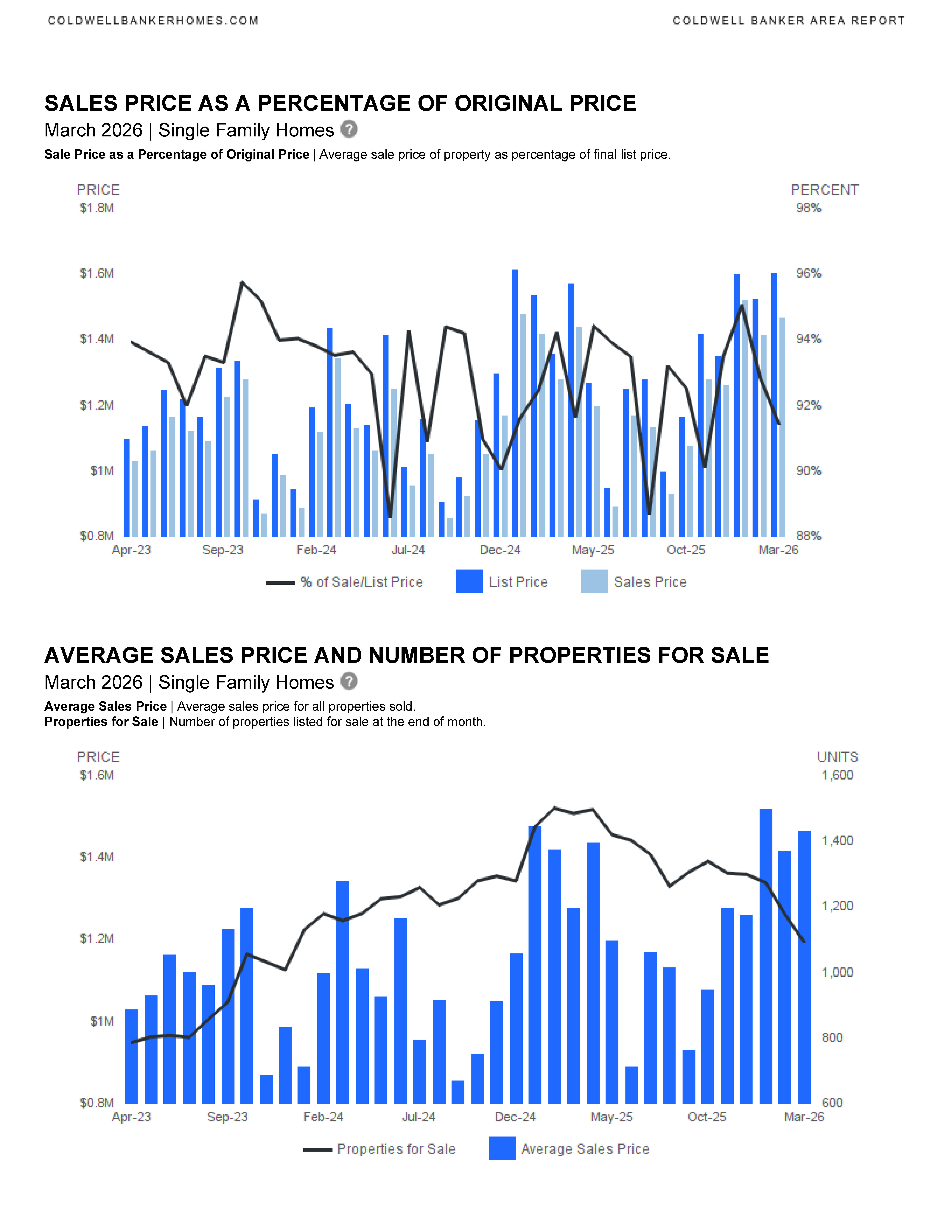

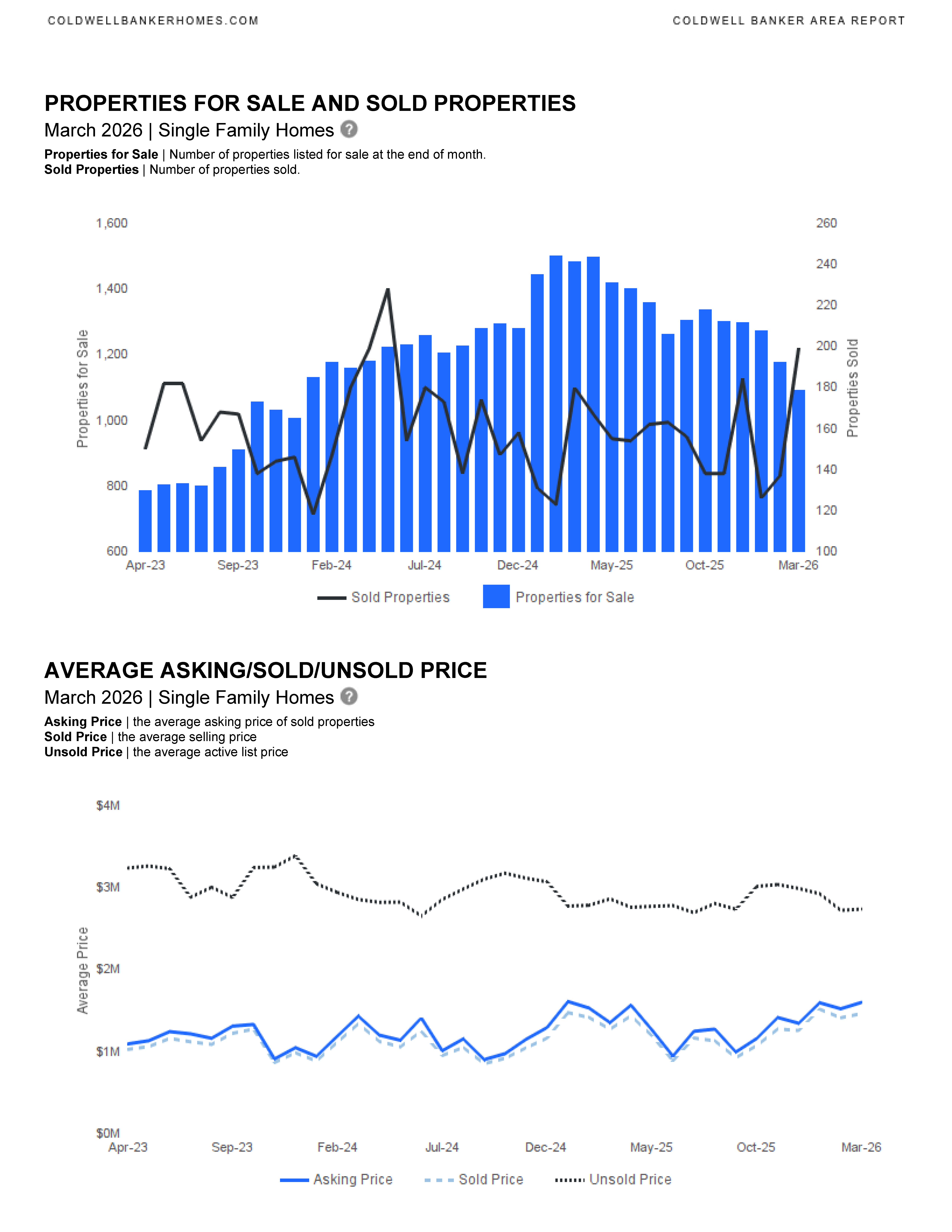

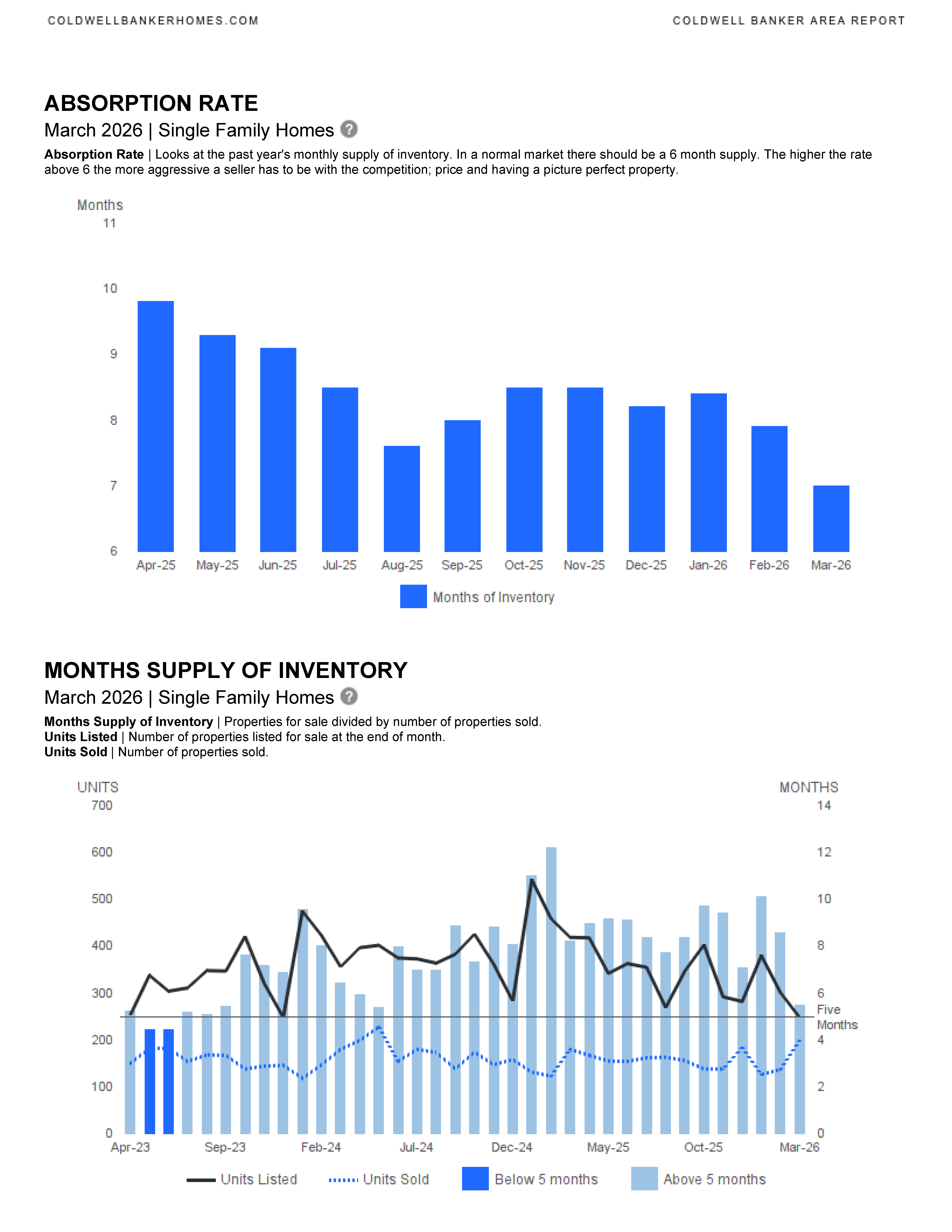

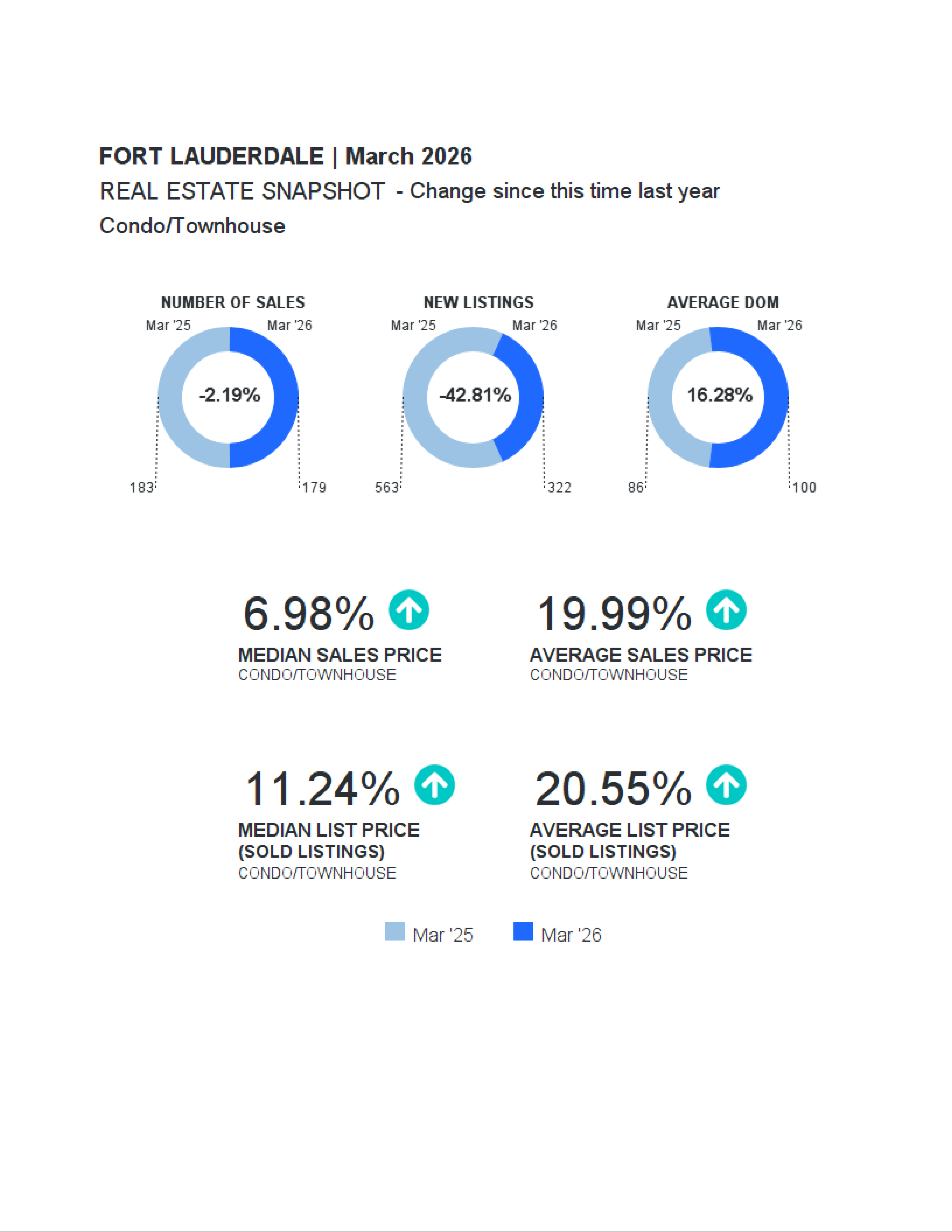

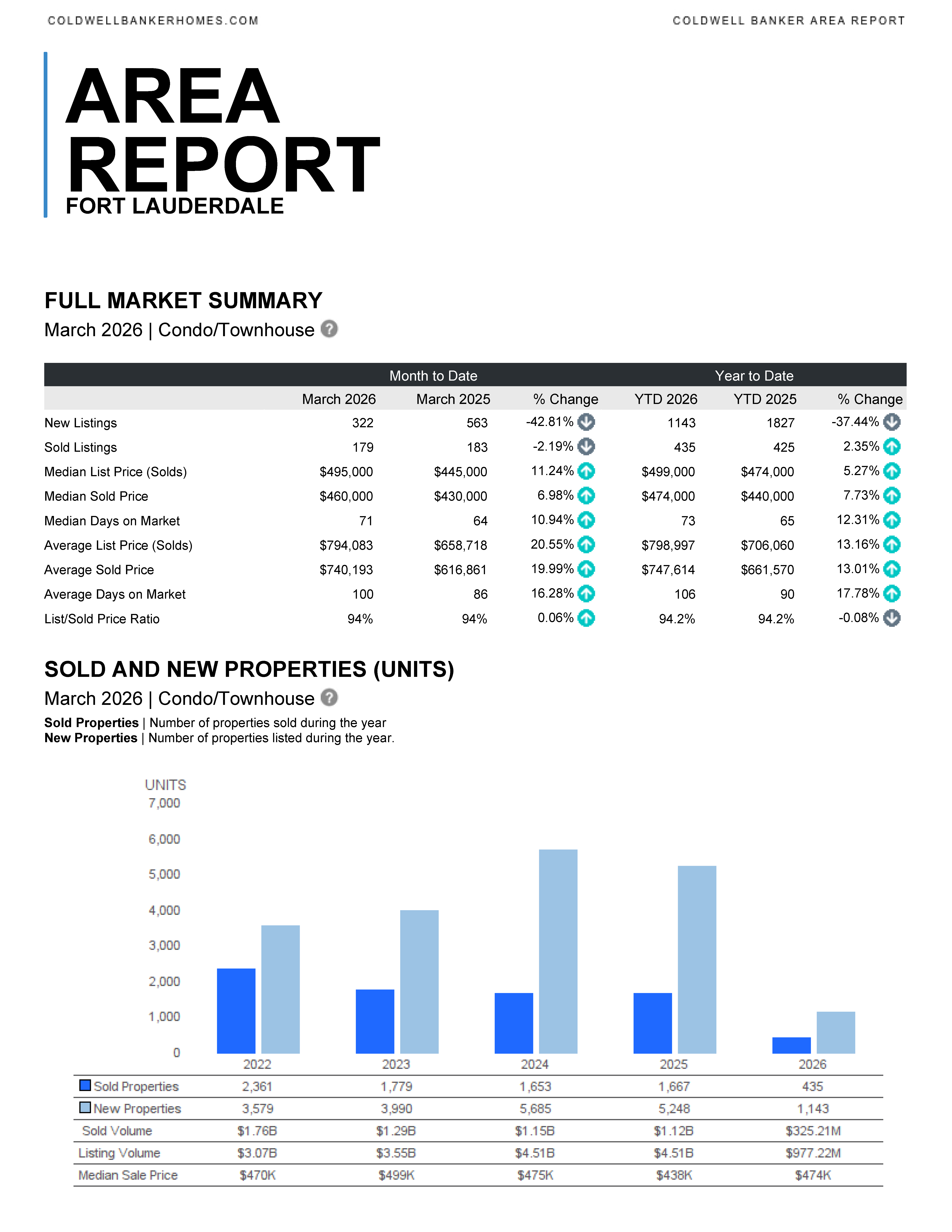

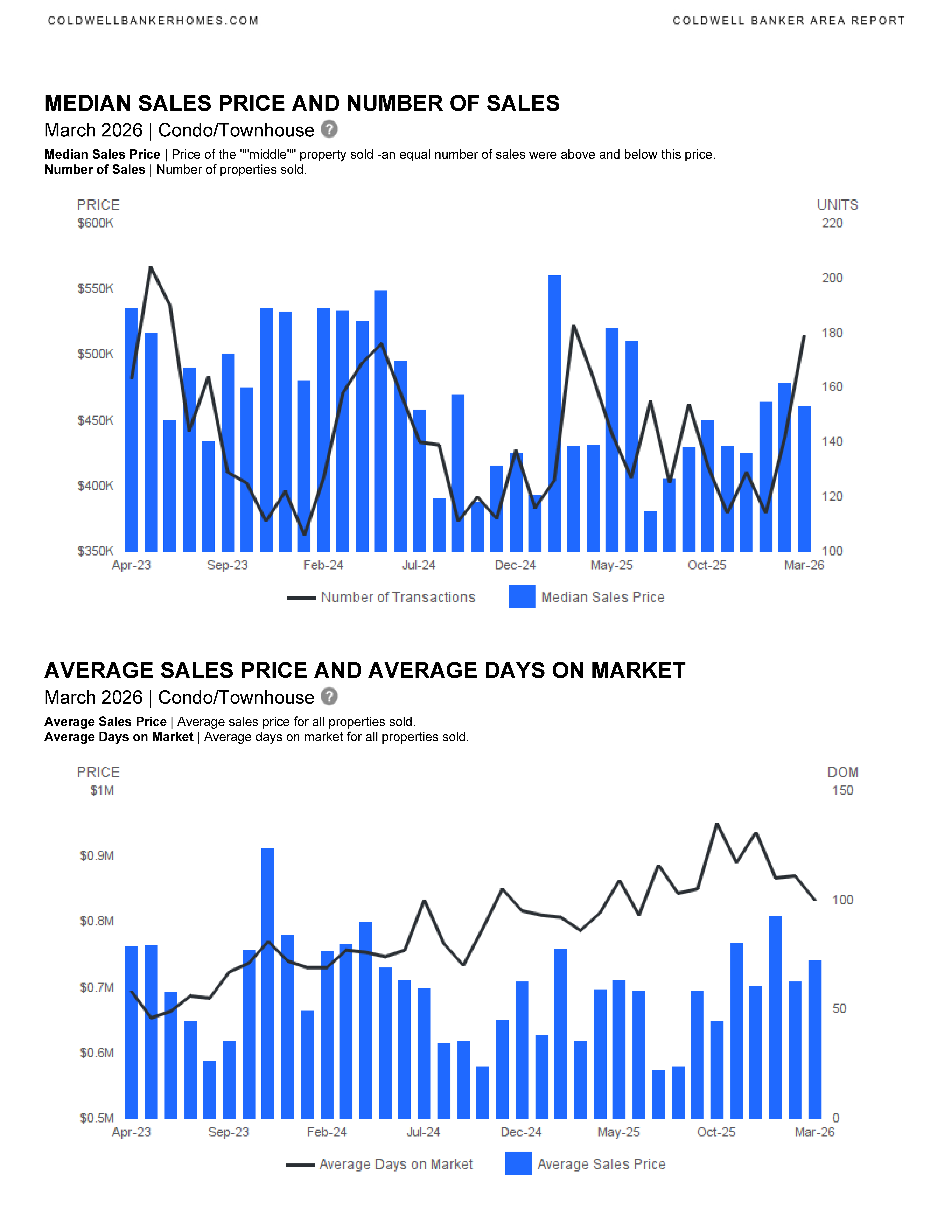

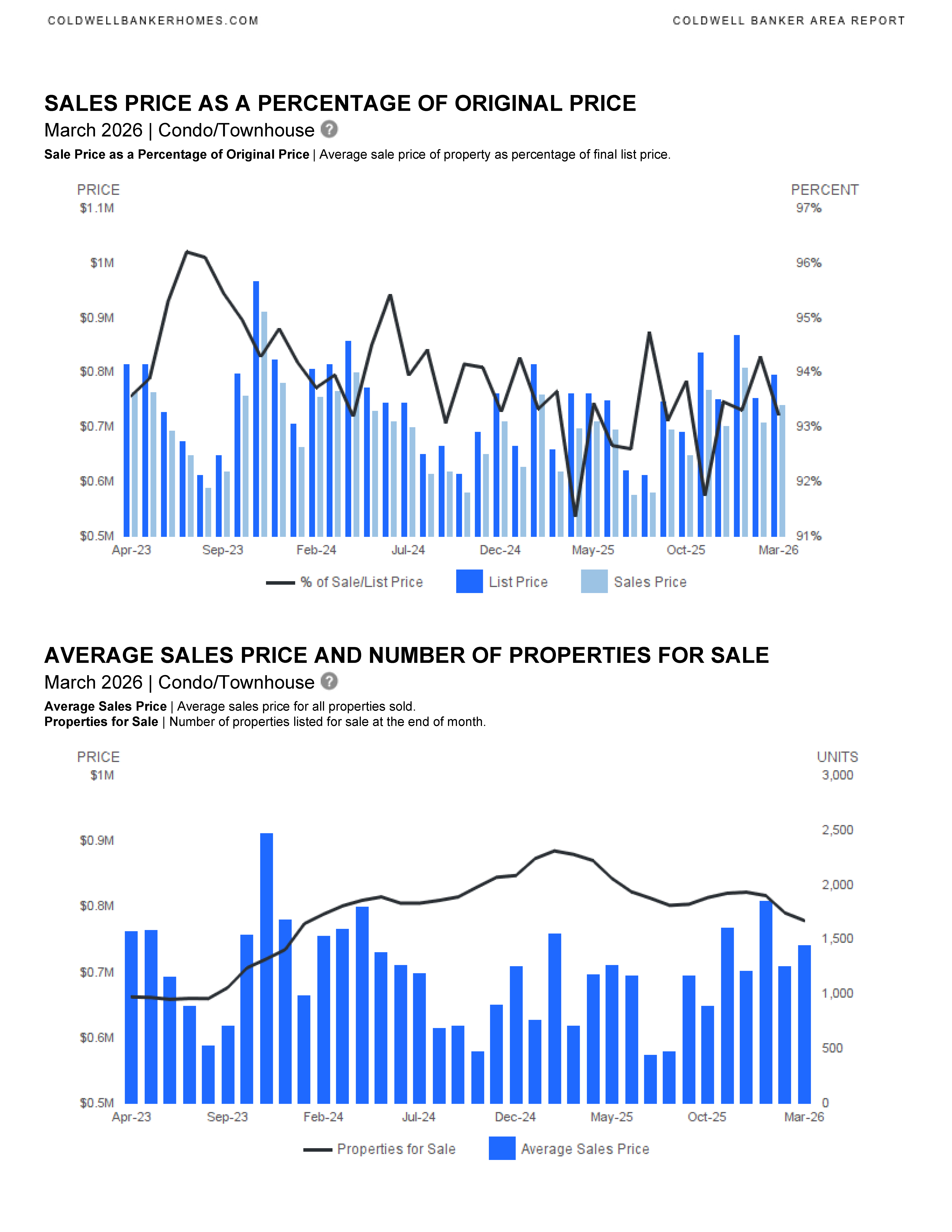

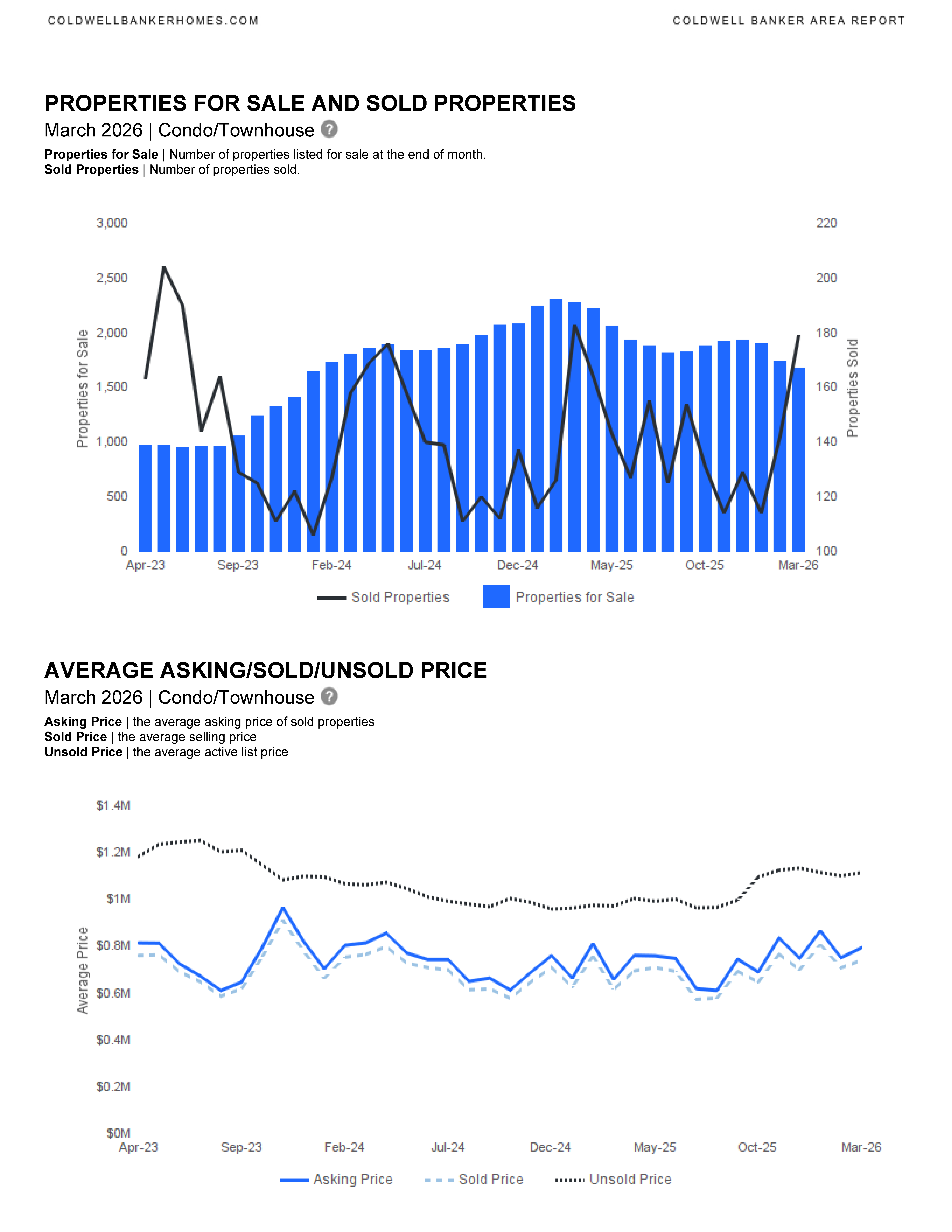

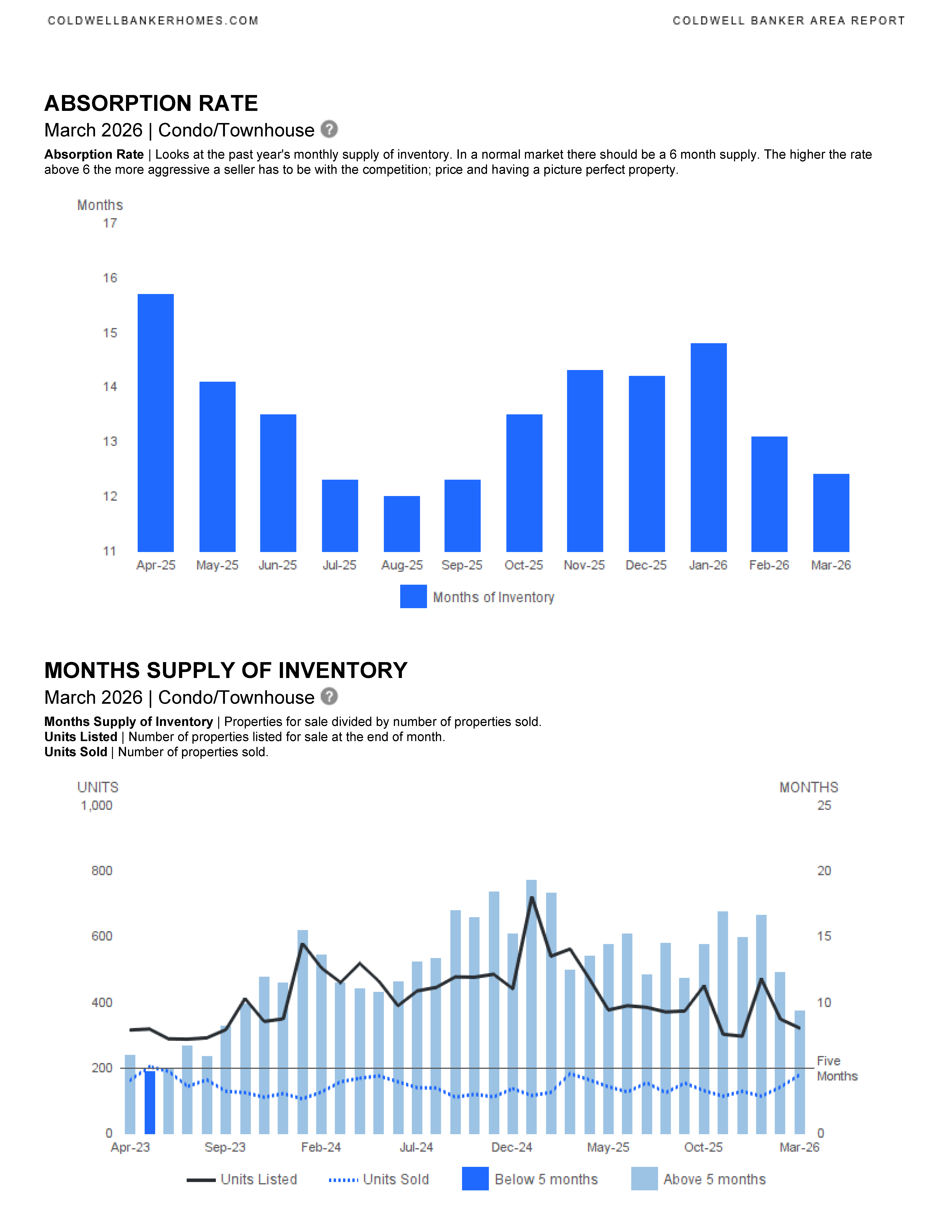

Fort Lauderdale March 2026 Area Report

Fort Lauderdale March 2026 real estate statistics have been published.

Single Family Homes

Condominium & Townhouses

Fort Lauderdale Real Estate Market Update – March 2026

🏡 Single‑Family Homes Market Highlights

- New listings declined sharply: 248 new listings, down 40.8% year over year

- Sales activity increased: 199 homes sold, up 10.6% compared to March 2025

- Median sold price softened: $575,000, down 5.1% year over year

- Homes are taking longer to sell:

- Median days on market: 61 days (+32.6%)

- Average days on market: 91 days (+30%)

- High-end activity remains strong:

- Average sold price rose 14.8% to $1.46M

- Pricing adjustments evident:

- List-to-sold price ratio dipped to 94.1%

🏢 Condo & Townhome Market Highlights

- Inventory tightened significantly:

- New listings down 42.8% year over year

- Sales remained steady:

- 179 units sold (nearly flat vs. last year)

- Prices continue to rise:

- Median sold price: $460,000 (+7.0%)

- Average sold price: $740,193 (+20.0%)

- Longer selling timelines:

- Median days on market increased to 71 days

- Stable pricing power:

- List-to-sold price ratio held at 94%

📊 Market Trends to Watch

- Inventory is constrained across both property types, especially condos

- Buyers are taking more time, signaling a more balanced market

- Luxury and higher-priced segments remain resilient

- Price growth is strongest in the condo/townhome sector

✅ Quick Market Takeaway

The Fort Lauderdale real estate market in March 2026 reflects a shift toward balance. Fewer new listings and longer days on market indicate cooling momentum, yet strong sales activity and rising average prices—especially in condos—show continued buyer confidence. Sellers benefit most when homes are priced strategically, while buyers are gaining slightly more negotiating power.

In this housing market in SE Florida, you need to work with an experienced and knowledgeable real estate professional. Please contact me if you would like to be sent updated market reports for YOUR specific neighborhood, Fort Lauderdale, or another SE Florida city. We can discuss the market, current trends and how we can work together to accomplish your real estate goals. I am here to help.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

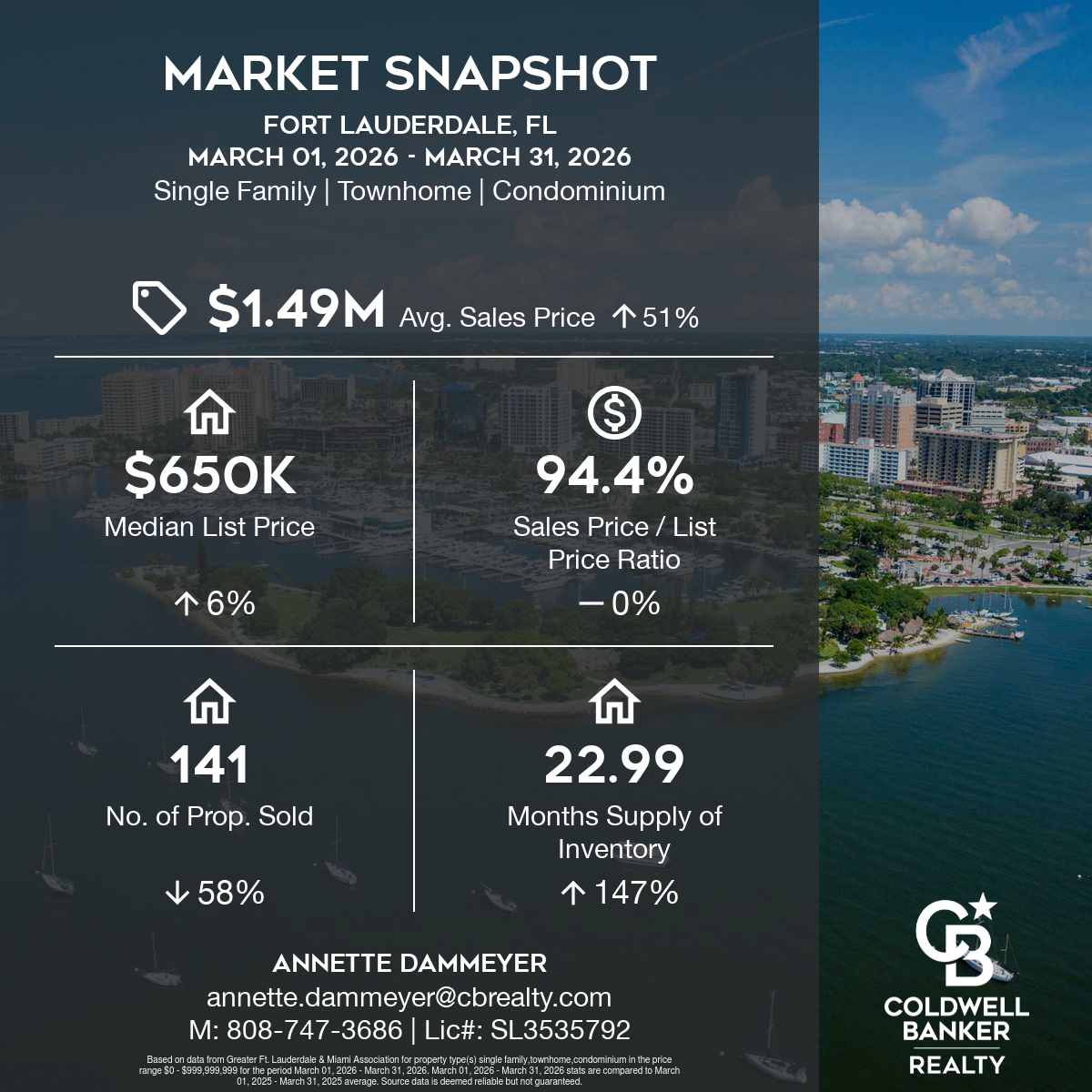

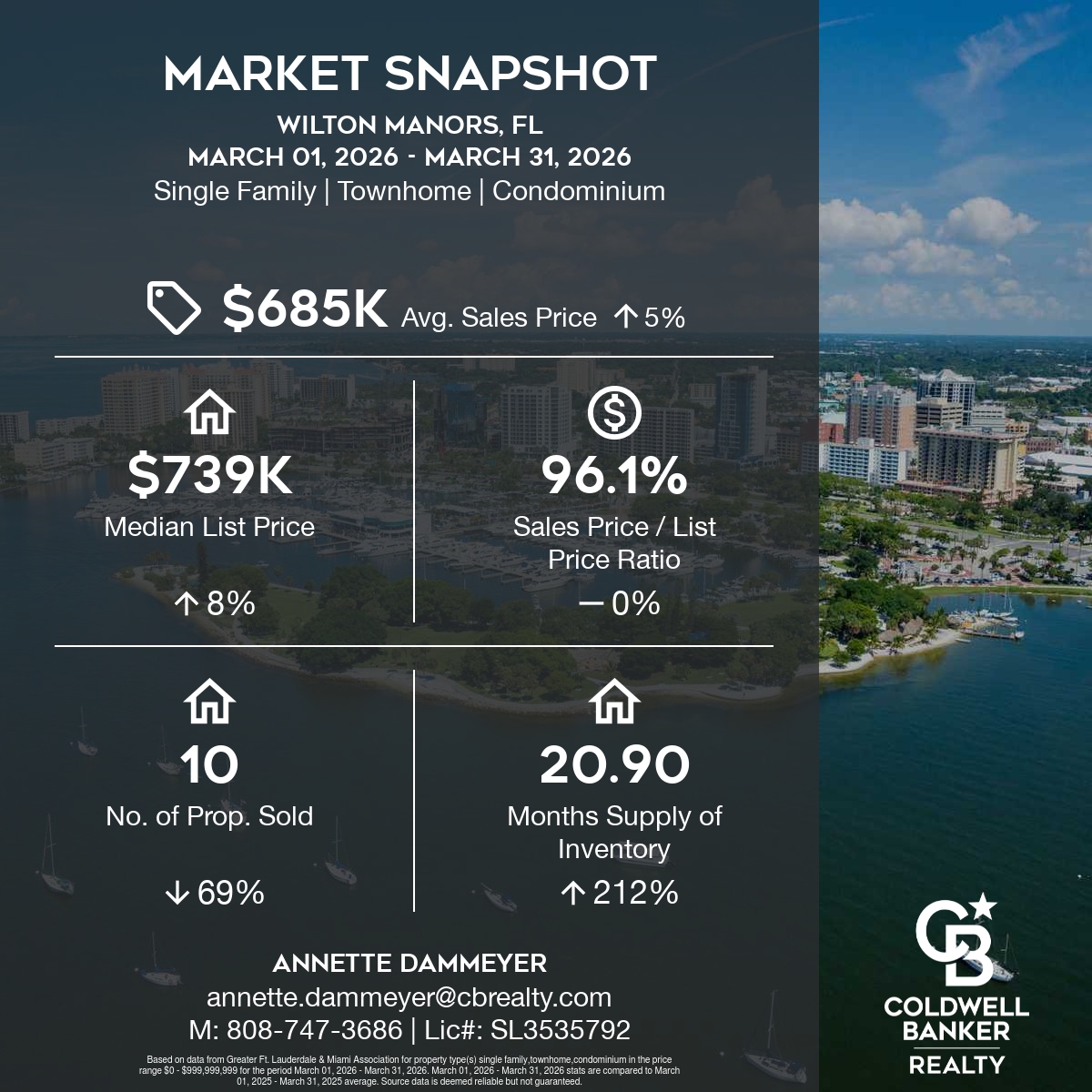

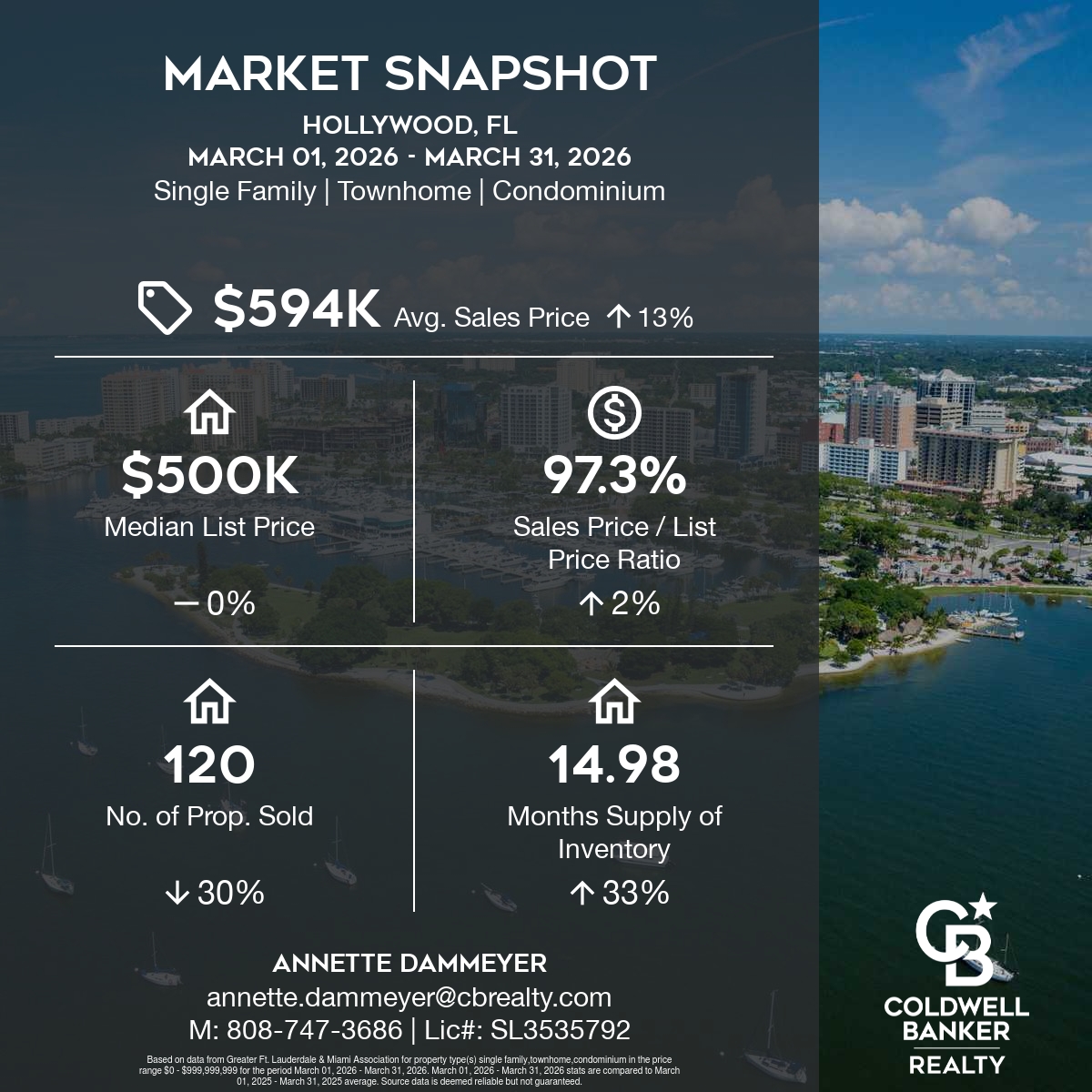

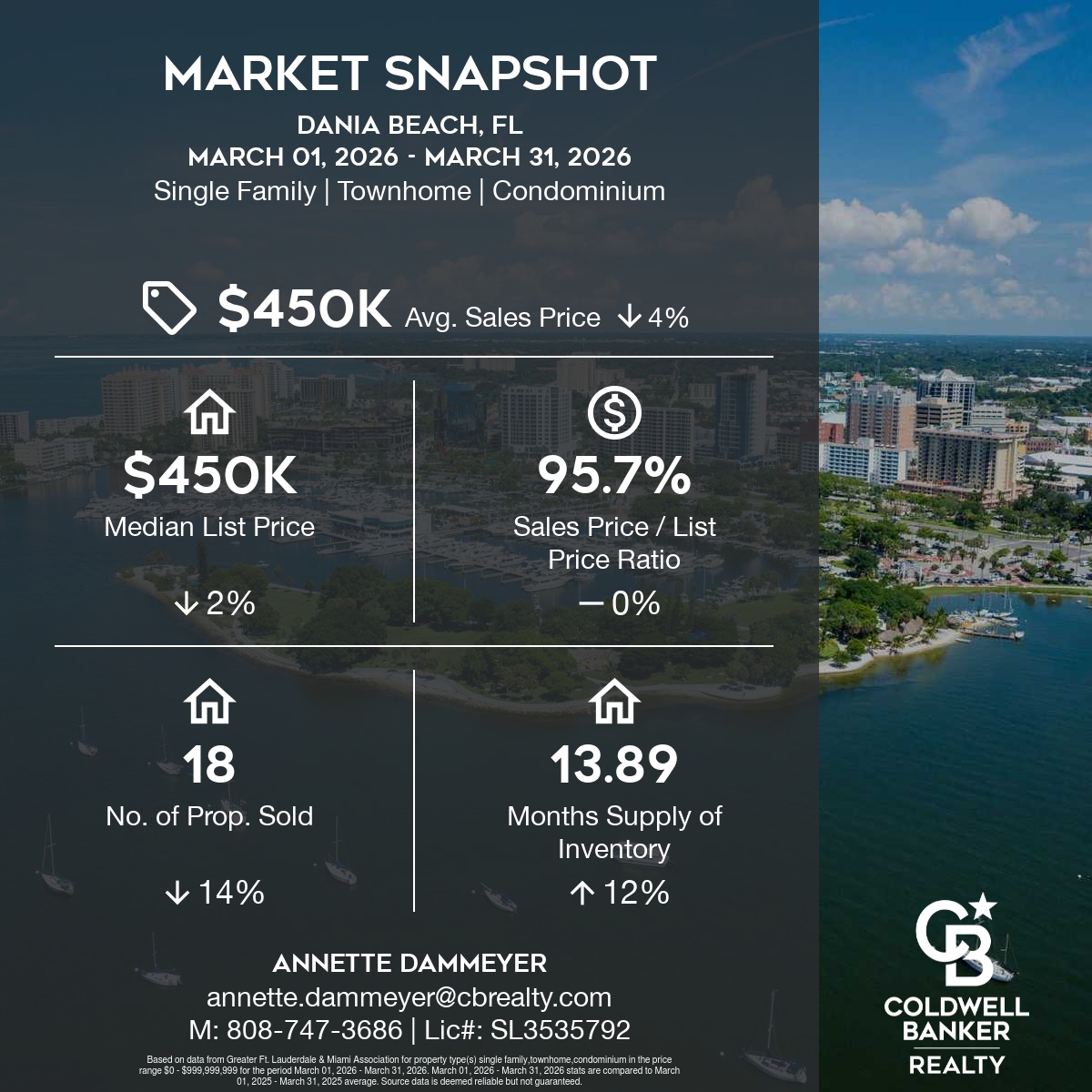

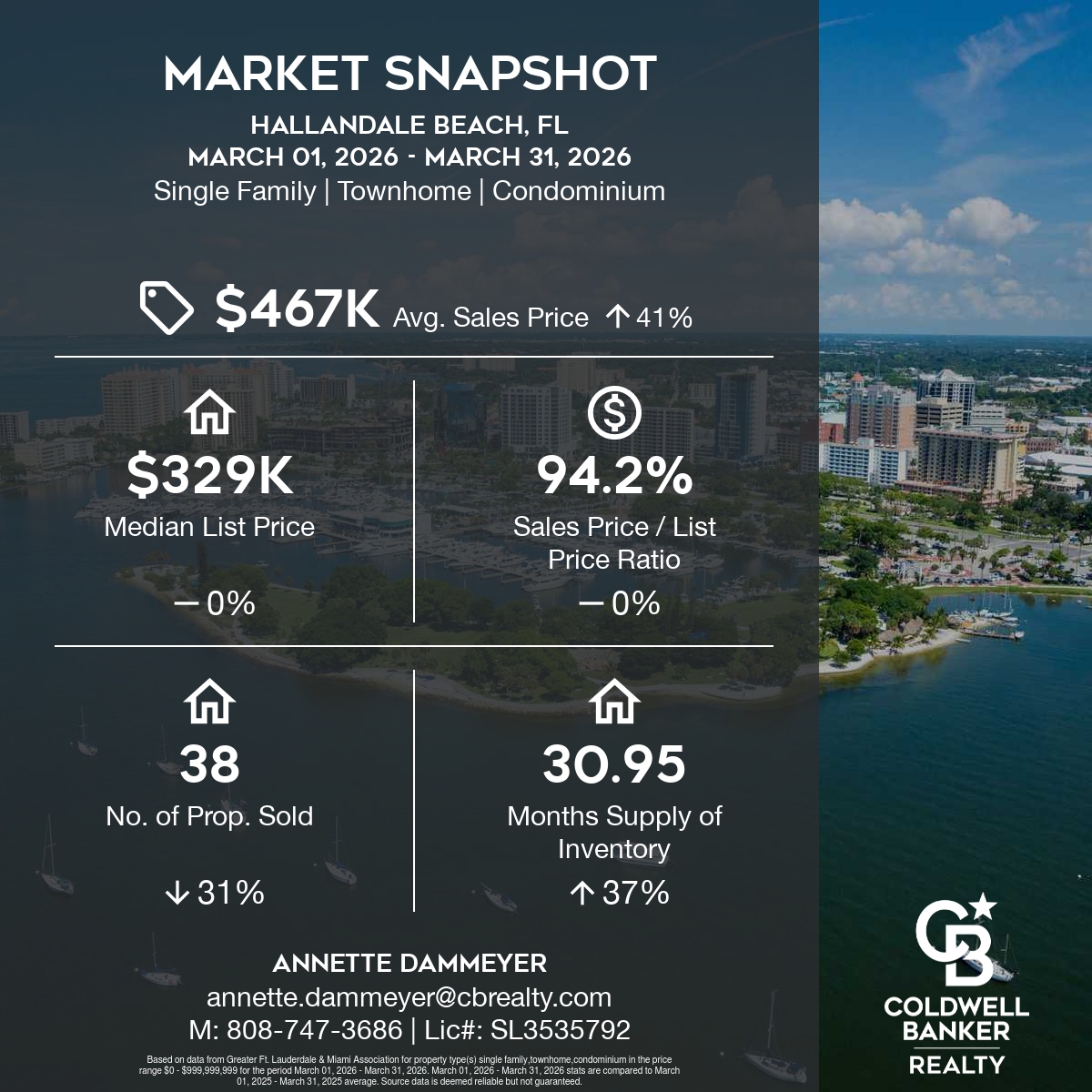

SE Florida Market Snapshot – March 2026

Market Trends in SE Florida

The real estate market is adjusting. With the fluctuation in property inventory, SE Florida is leaning towards a “buyer’s market”. Seller’s are now reassessing their asking price on their properties for sale. It is crucial to examine other similar homes on the market to establish an aggressive original listing price, generating multiple buyer’s attention to your property. This is also an important time to consider a decrease in asking price if the property has been on the market without active offers. I welcome any discussions you may want to have regarding your neighborhood trends. Please reach out to chat, even if you are not ready to buy or sell, but just would like to discuss current real estate updates. Here are the Market Snapshots reflecting the last month (compared to the same month last year) for the following areas:

- Fort Lauderdale

- Wilton Manors

- Hollywood

- Dania Beach

- Hallandale Beach

These take into account all property types (Single Family Homes/Condos/Townhomes).

The real estate landscape in South Florida is evolving. Making smart, timely decisions has never been more important. Whether you’re considering selling, buying, or simply staying informed, I’m here to be your local advisor and resource.

Let’s talk about current market trends and how we can align your goals with today’s opportunities. I’d be happy to provide customized market reports for Fort Lauderdale, any SE Florida city, or even your specific neighborhood—all automatically delivered to your inbox.

Call or email me anytime. I’m here to help you move forward with clarity and confidence.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

April 2026 ~ Goldilocks Window, Spring Cleaning and Impactful Landscaping

April 2026 NewsletterWelcome to Your April 2026 Real Estate & Lifestyle Update!As we step into one of the most vibrant seasons here in Southeast Florida, I’m excited to share timely information to help you stay informed, empowered, and inspired in today’s dynamic real estate landscape. This month’s issue is packed with value: 1) Prime Spring Selling Window in SE Florida 2) The Ultimate Spring Cleaning Checklist 3) Landscaping Upgrades That Make the Biggest Impact 4) Celebrating Fair Housing Month Plus: Your Local Area Market Reports Happy Spring, |

|||||||||||

National Stories

|

|||||||||||

Real Estate Updates | Area Reports | February 2026

|

If you’re considering selling, now is the perfect time to start preparing for a strategic April–May launch. Your Goldilocks moment is just ahead—let’s make sure your home shines when it counts most. Spring brings stronger demand, beautiful curb appeal, and the ideal mix of timing and market momentum. Ready to make your move? Let’s get your home market‑ready. 💫

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

![]()

Prime Spring Window For Sellers

The “Goldilocks” Moment: Why April Through May Is the Perfect Time to Sell Your Southeast Florida Home

If you’re a Southeast Florida homeowner thinking about selling, choosing the right time to list your property can significantly affect your final sale price, days on market, and overall selling experience. In real estate, we call this the “Goldilocks period”—the window that’s not too early, not too late, but just right.

While timing varies across the country, here in Southeast Florida, our market follows a unique rhythm. And in today’s landscape, the strongest, most strategic selling window is April through May.

Let’s explore why this period delivers exceptional results, what drives the seasonal shift, and how Southeast Florida compares to national trends.

✅ Why Timing Matters More Than Ever

The decision of when to list is guided by measurable data such as:

- Active buyer demand

- Median sale price trends

- Days on market

- Competition from other sellers

- Price‑reduction frequency

- Seasonal and regional behavior

Choosing the ideal timing helps ensure your home hits the market when buyers are energized, inventory is favorable, and your property achieves maximum visibility and value.

✅ Why April Through May Is the New Goldilocks Window in Southeast Florida

Historically, early spring marks the beginning of peak real estate activity across much of the United States—but in Southeast Florida, we now see April and May emerging as the most balanced, best‑performing months for sellers.

Here’s why:

- Strong Buyer Activity Ramps Up

By April, Southeast Florida experiences a surge of touring activity.

Tourists are still visiting, seasonal residents are still in town, and northern buyers continue to escape extended cold seasons and late spring storms up north. This creates one of the highest concentrations of active, motivated buyers you’ll see all year.

- Homes Show Exceptionally Well

April and May deliver some of the best showing conditions of the year:

- Lush landscaping

- Longer daylight hours

- Bright natural light

- Warm (but not summer-hot) weather

Properties simply look better, and buyers respond accordingly.

- Competition Remains Manageable

Unlike early January to March, when many snowbird-oriented sellers list, April through May sees strong buyer engagement without a dramatic surge in new listings, helping your home stand out.

- Strong Pricing Season

Nationwide, spring consistently yields the highest sale prices of the year—specifically in April and May. Southeast Florida mirrors this trend, with April and May producing strong offers and fewer price reductions compared to late summer and fall.

- Buyers Want to Close Before Summer

Families planning a summer move start shopping in earnest in April and May.

Investors also target this period to prepare for summer rental demand.

This creates urgency—and urgency supports stronger offers.

✅ Southeast Florida vs. the Rest of the Nation

Nationally, research shows that spring is the strongest season, with April often considered the prime selling month and May delivering some of the year’s highest premiums.

The National Trend

- Buyers return to the market after winter slowdowns

- Prices peak in late spring

- Homes sell faster with fewer price cuts

- Curb appeal improves across the country

Southeast Florida’s Advantage

While our local early-year activity is strong, April and May combine the best of all worlds:

- High-quality buyers still in-state

- End-of-season snowbirds ready to purchase before heading home

- Northern buyers experiencing late winter/spring chill

- Aesthetic peak of Florida curb appeal

- Reduced competition versus earlier months

This positions Southeast Florida sellers to maximize price and minimize time on market.

✅ The Outcomes of Selling Strategically in April–May

When you list your home during this Goldilocks window, you can expect:

✔ Stronger Offers

Buyers are financially ready, emotionally motivated, and competing for a limited number of well-presented homes.

✔ Faster Sales

Properties listed in spring tend to spend fewer days on market because buyer urgency and touring activity are at their peak.

✔ Higher Net Proceeds

Spring listings historically produce higher sale prices and fewer price reductions than homes listed later in the year.

✔ Better Marketing Performance

Your home benefits from the natural beauty of spring, extended daylight hours, and a larger audience of local, national, and international buyers.

✅ So, When Should You List?

For 2026 and beyond, Southeast Florida homeowners will find the optimal Goldilocks period is April 1 through May 31.

This window offers:

- The strongest blend of buyer demand and property presentation

- Favorable pricing trends

- Faster contract timelines

- A balanced level of competition

If you’re preparing to list, beginning your pre-market work in March ensures your home is perfectly positioned for the April–May peak.

📣 Ready to Make Your Move?

As your Southeast Florida agent, I’ll help you:

✅ Determine the ideal listing date for your neighborhood

✅ Prepare and stage your home for maximum impact

✅ Develop a tailored marketing strategy that attracts qualified buyers – https://annettedammeyer.com/marketing-strategy

✅ Secure the strongest possible offer in the optimal selling window

If you’re considering selling, now is the perfect time to start preparing for a strategic April–May launch. Your Goldilocks moment is just ahead—let’s make sure your home shines when it counts most.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

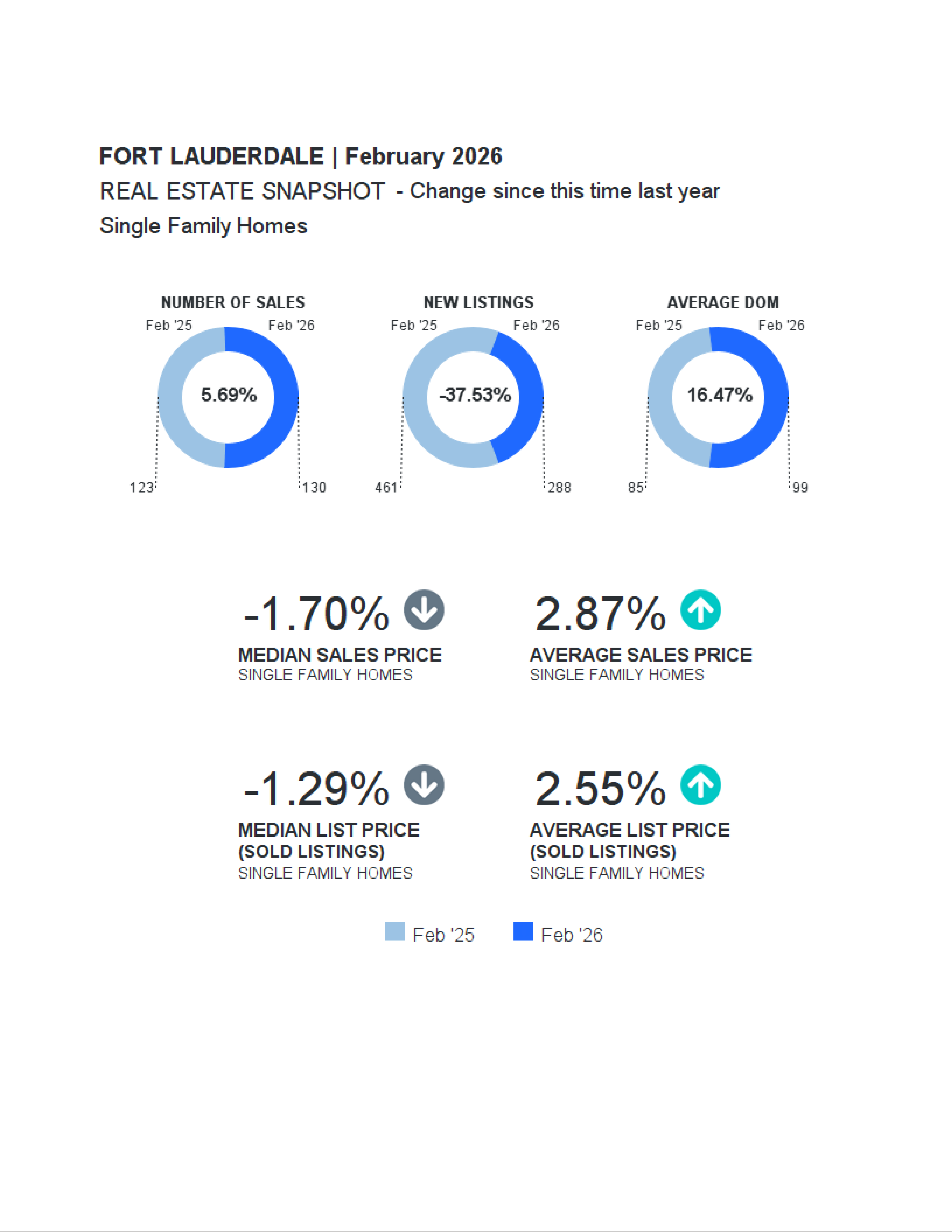

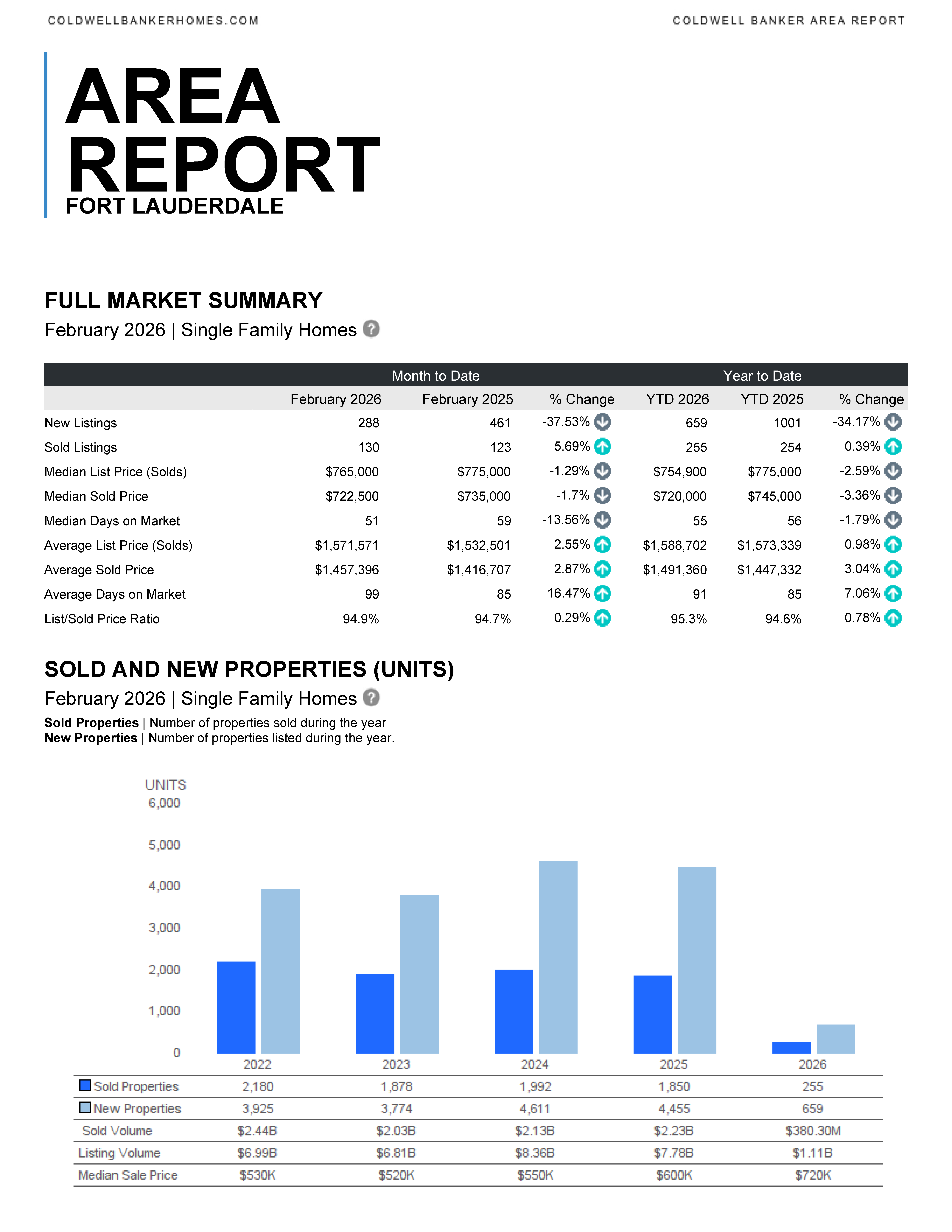

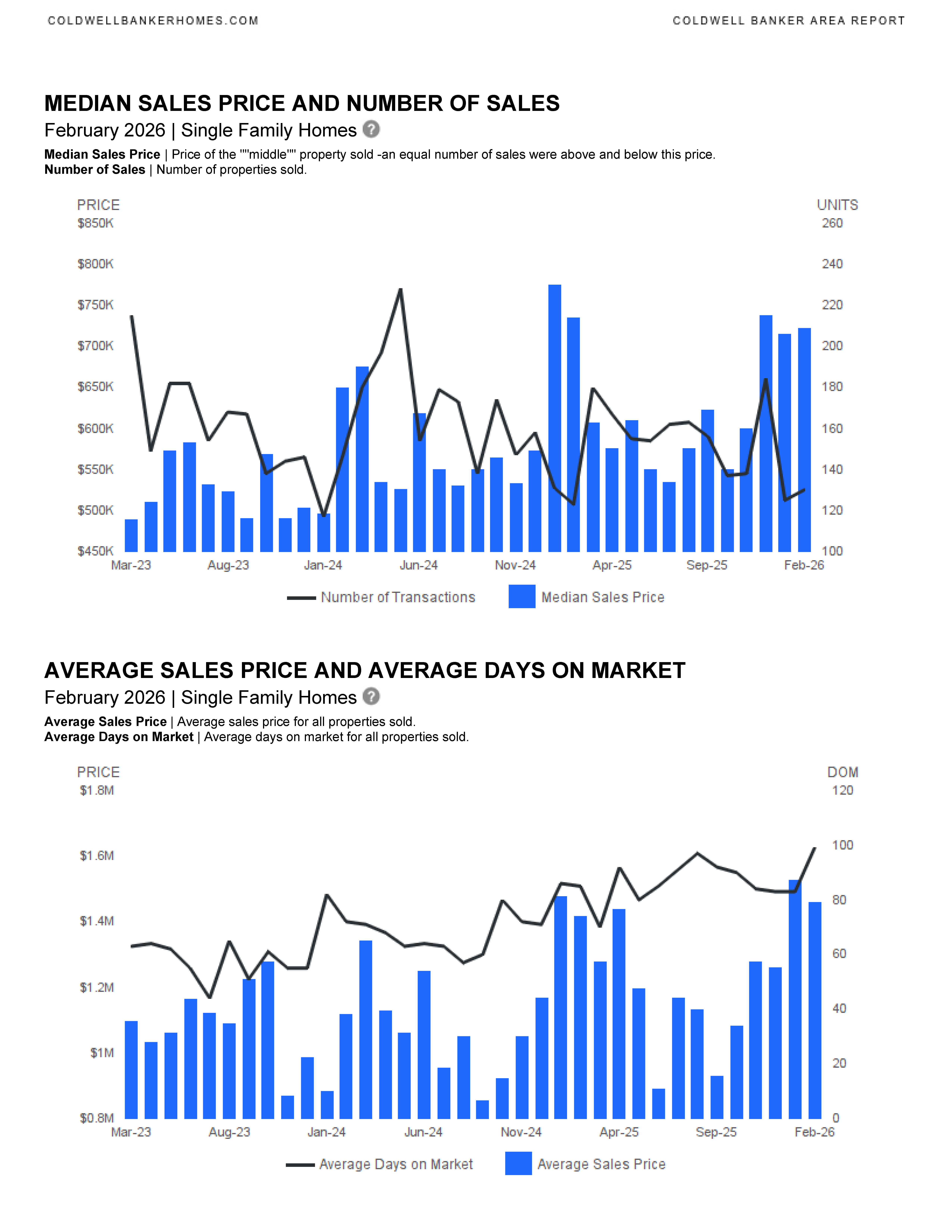

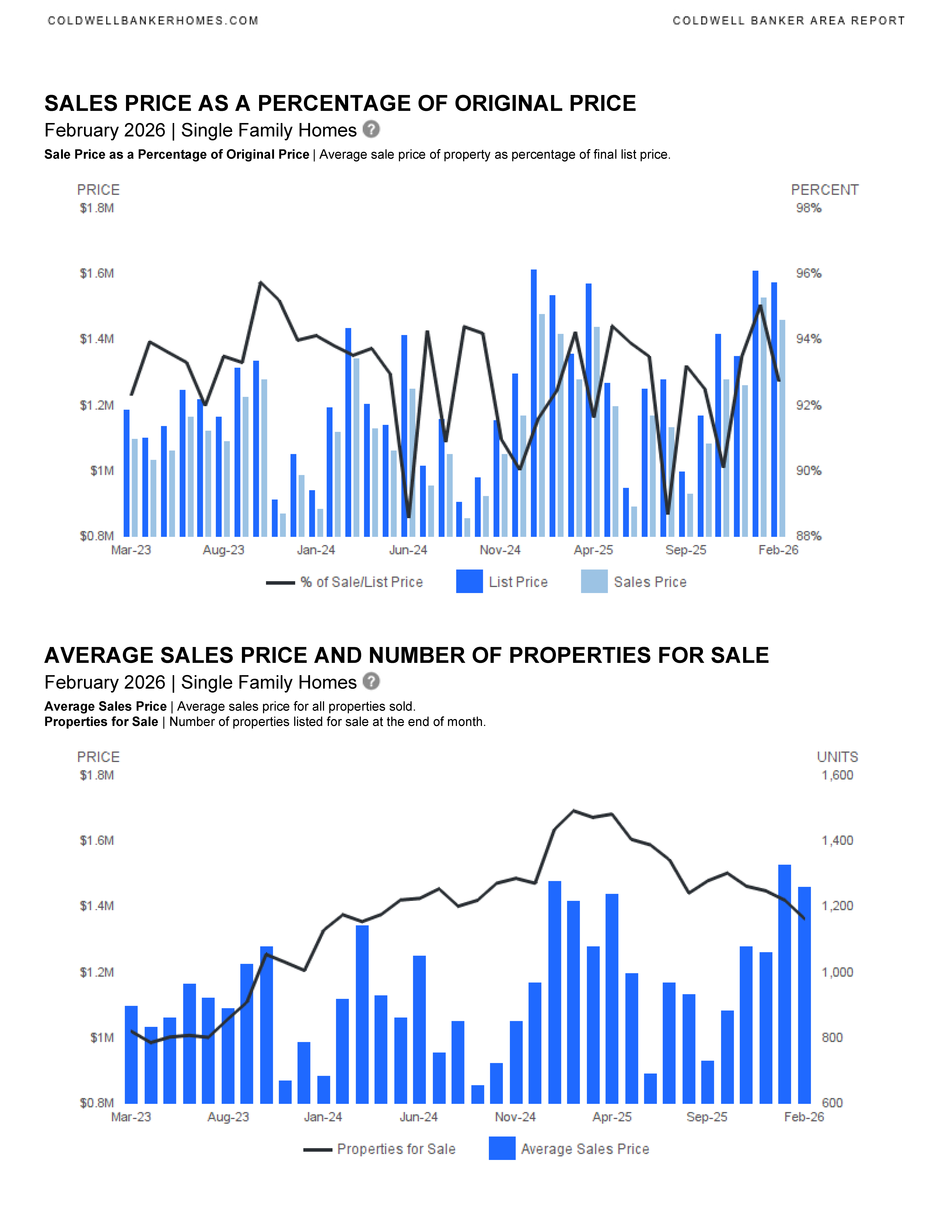

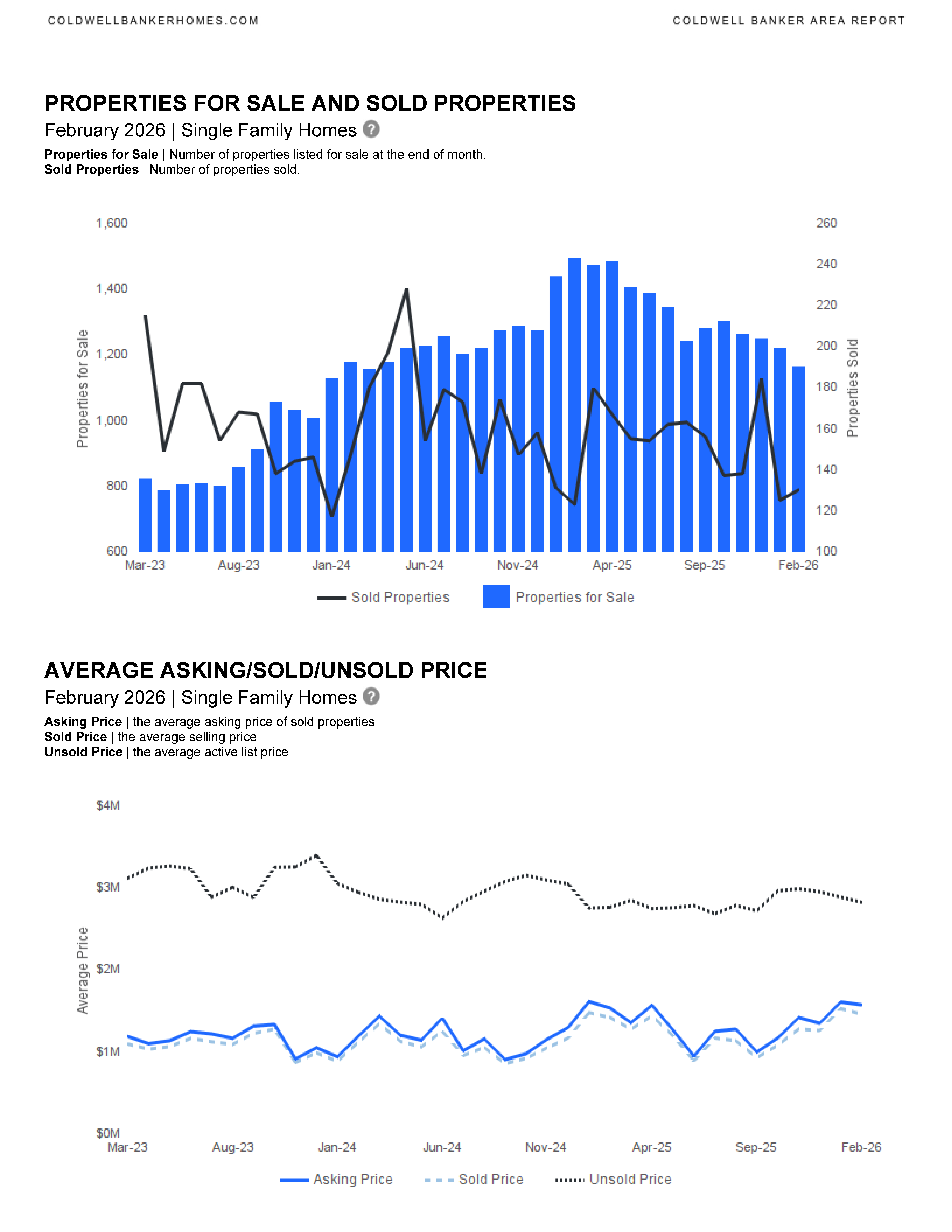

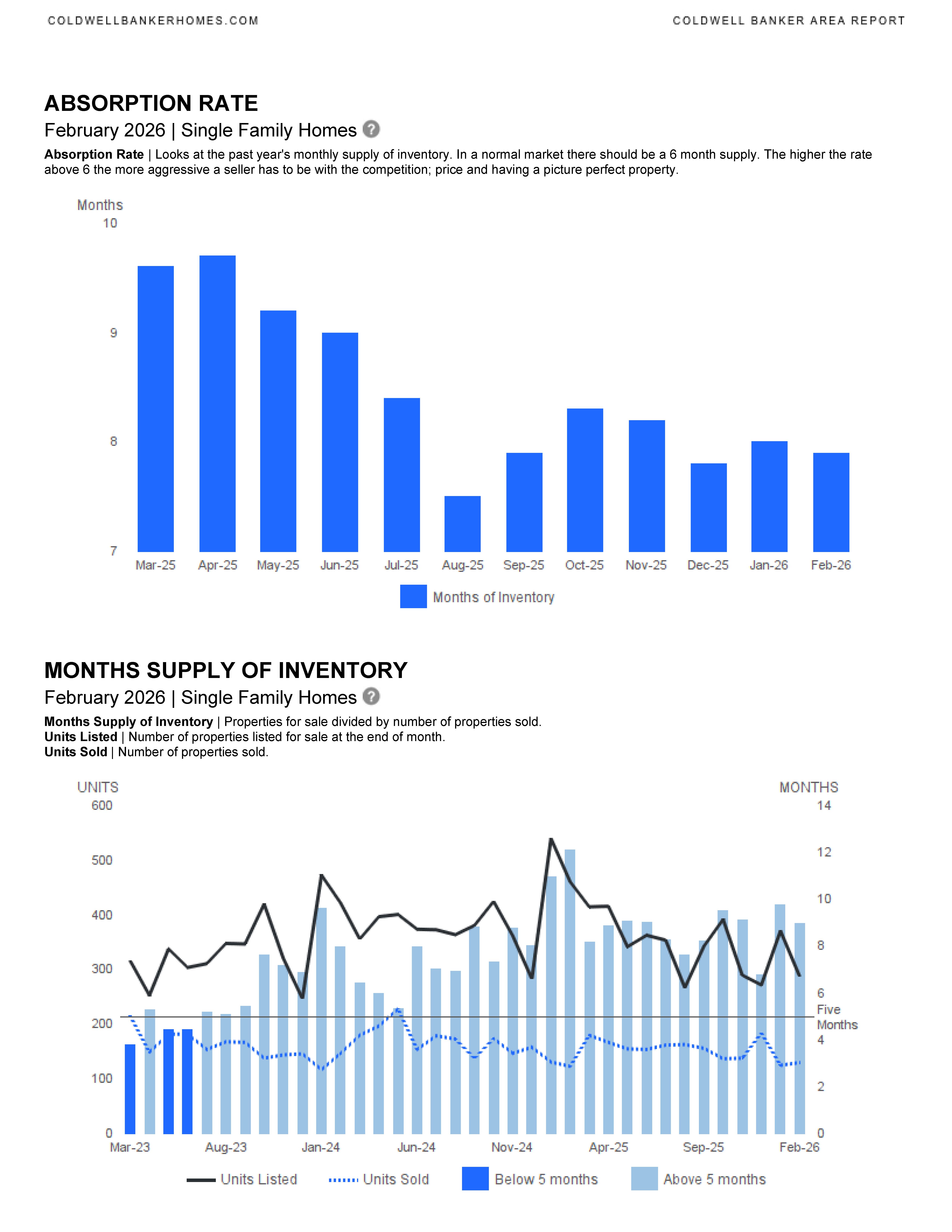

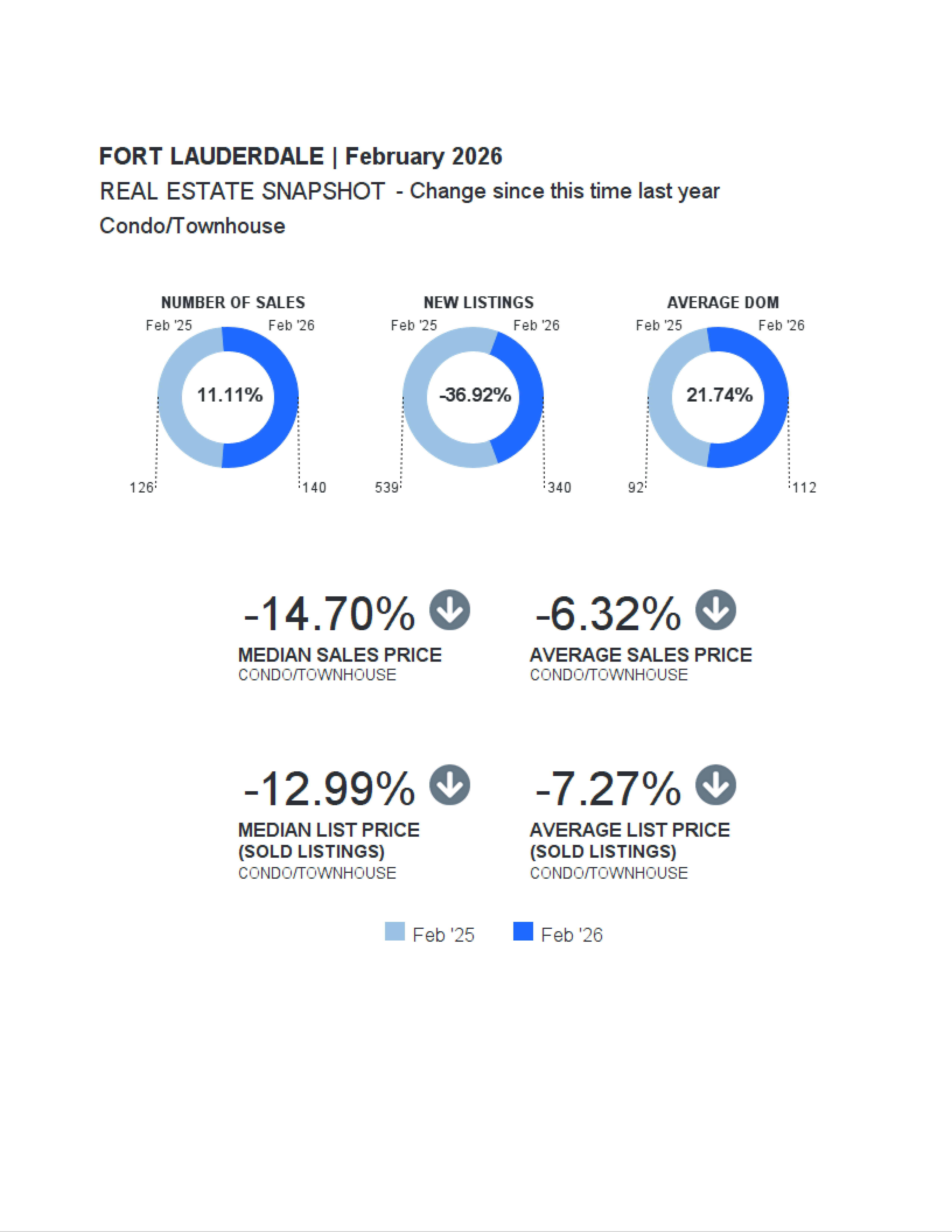

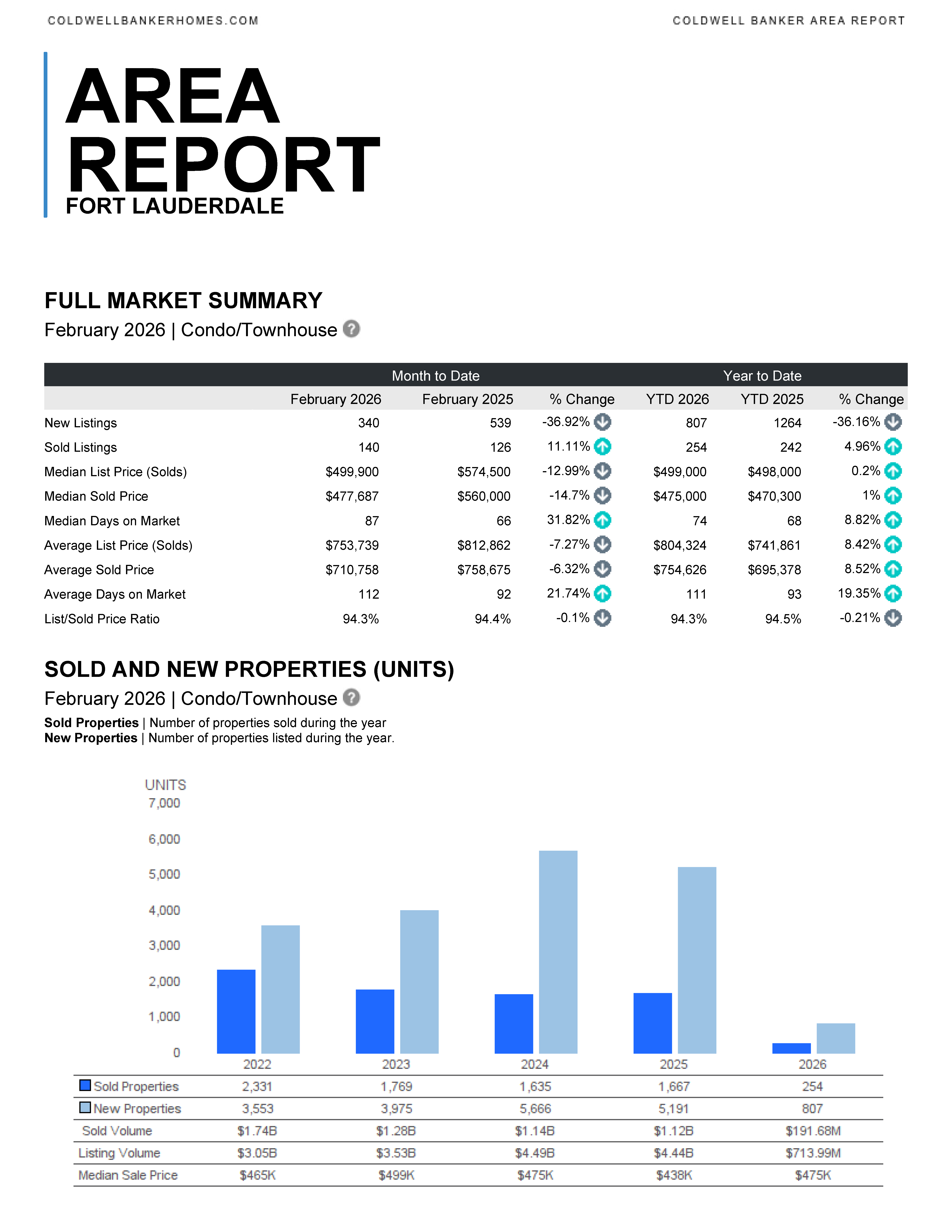

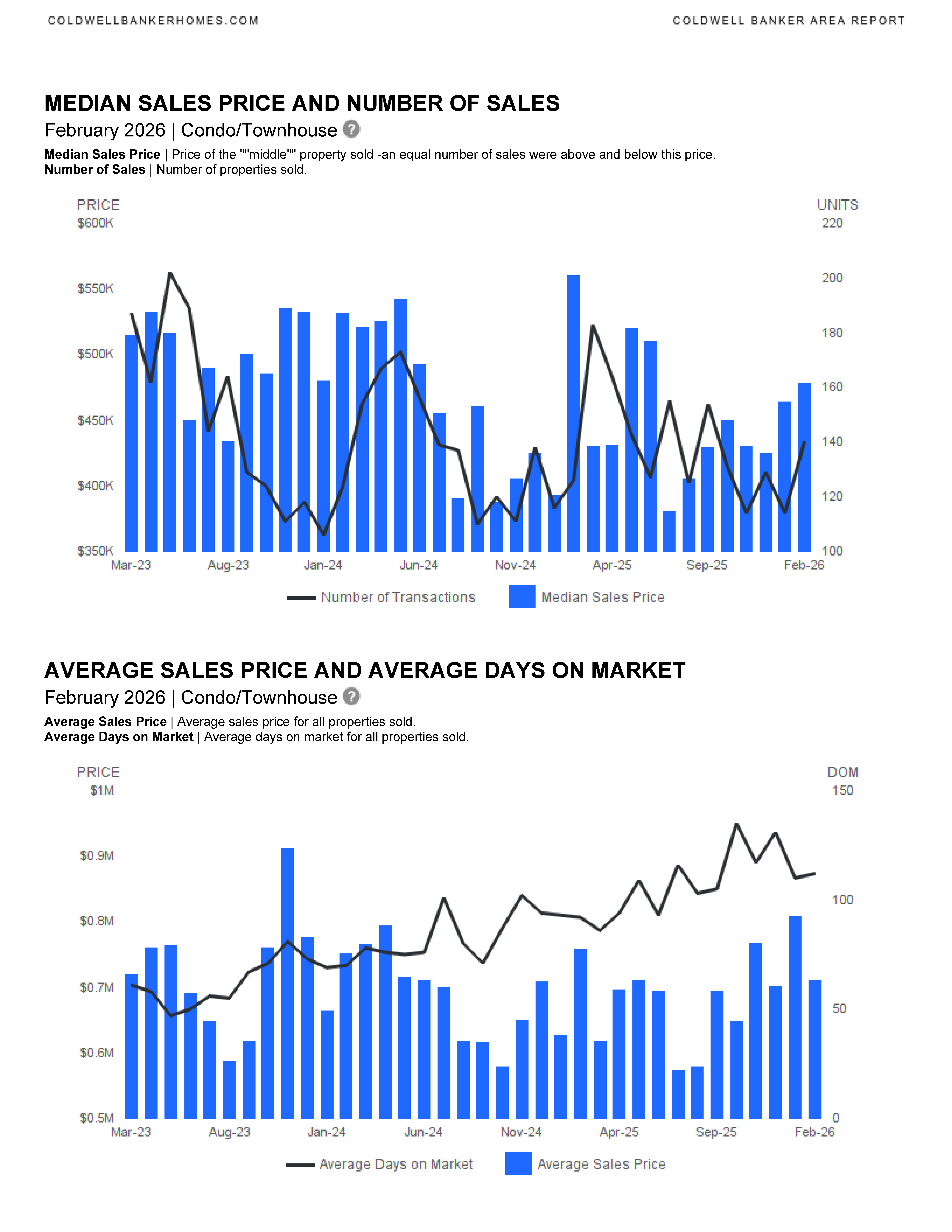

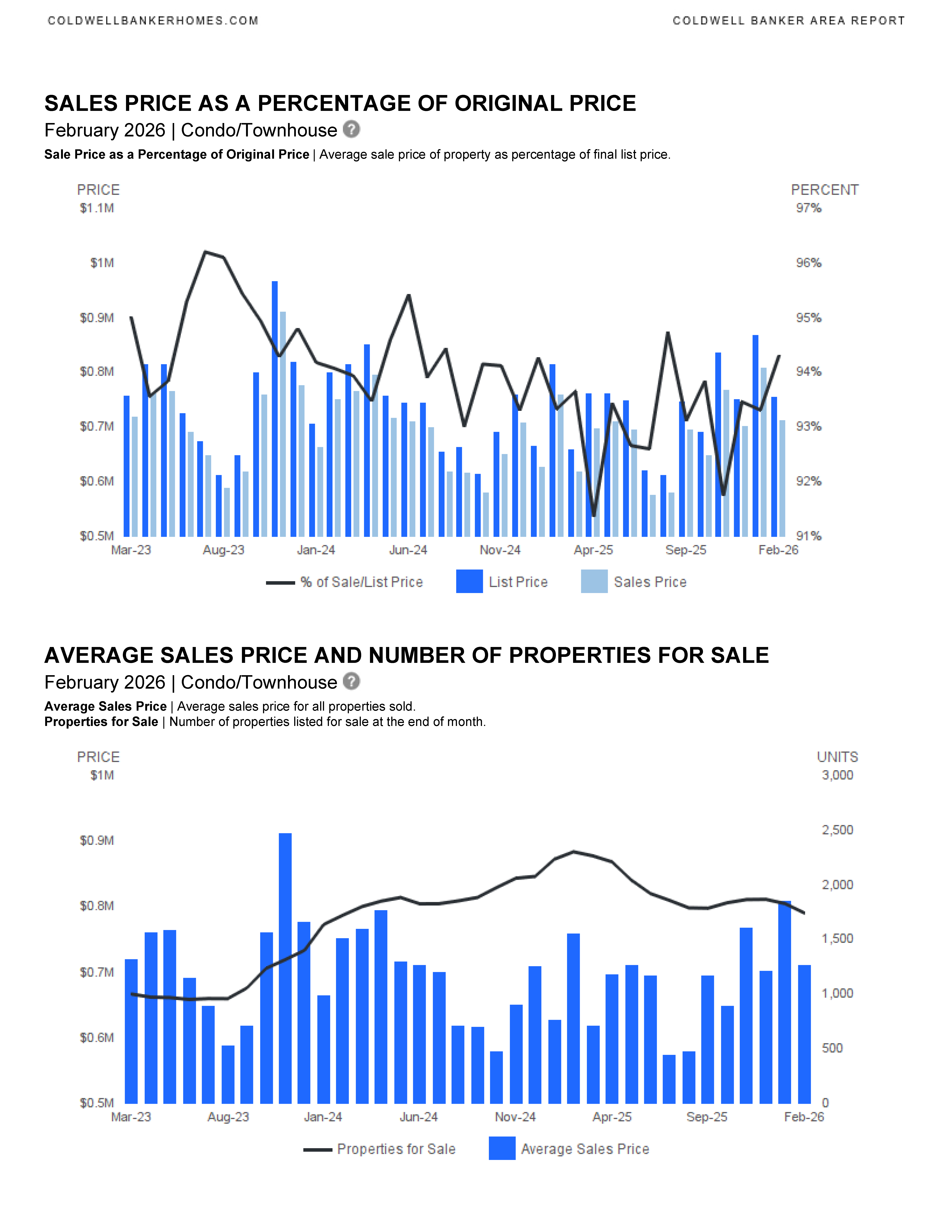

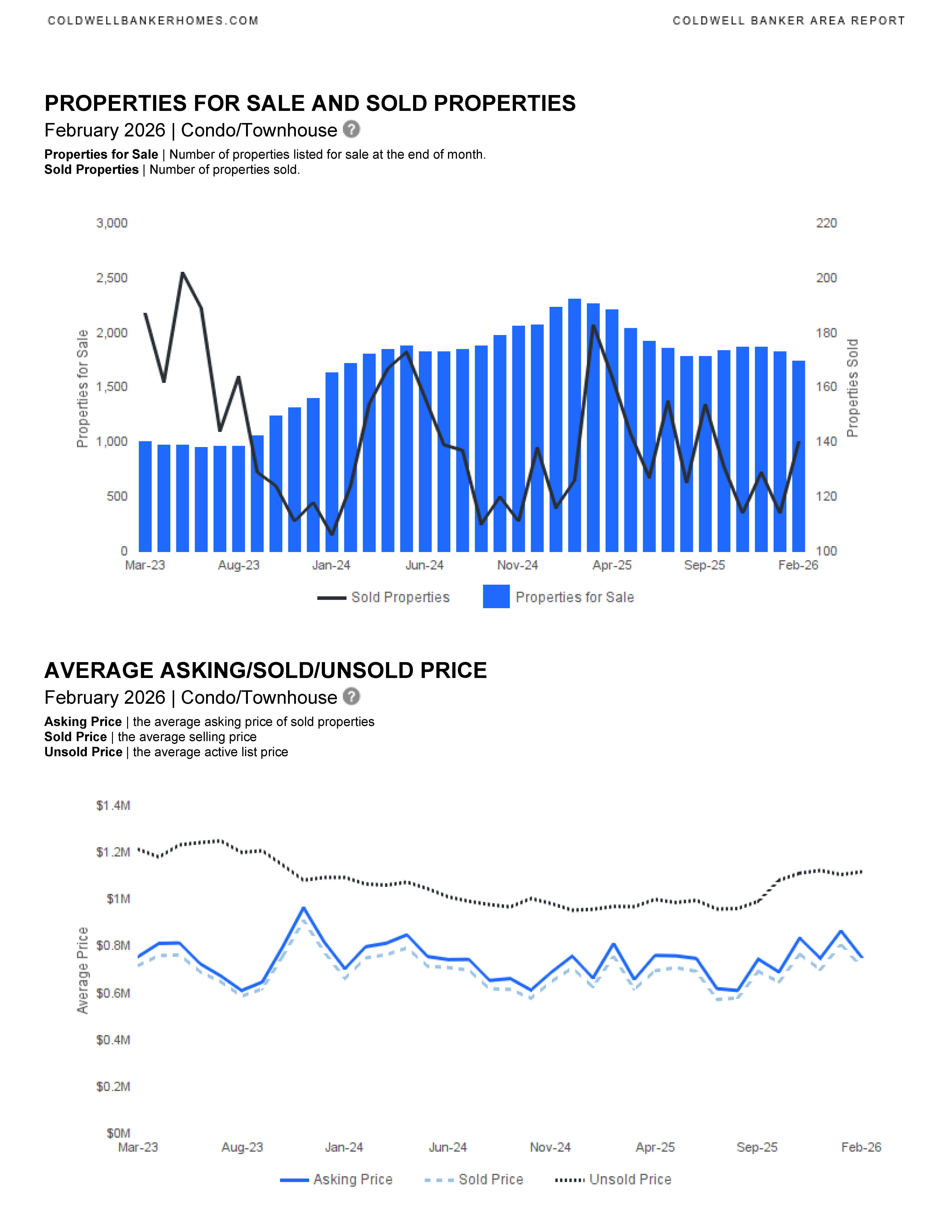

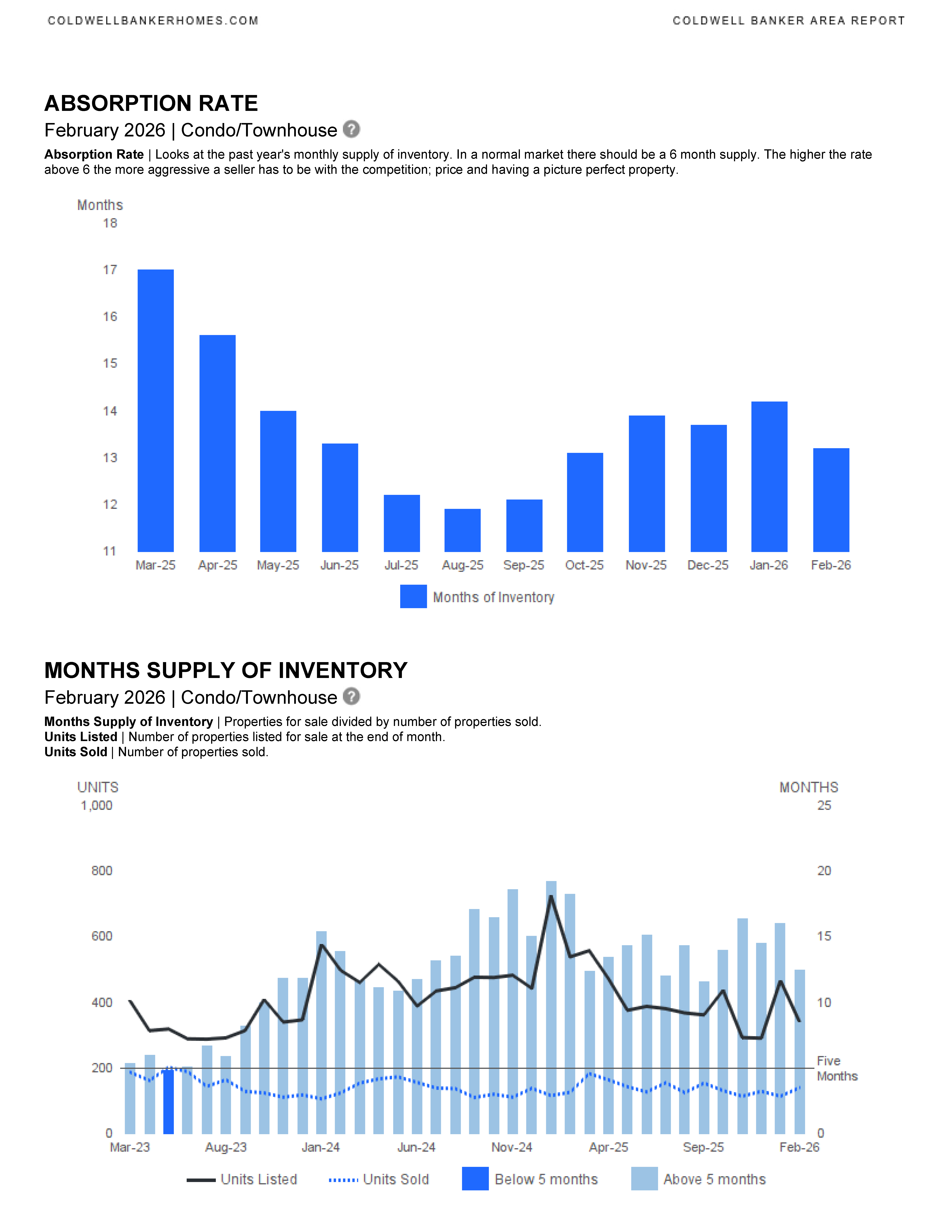

Fort Lauderdale February 2026 Area Report

Fort Lauderdale February 2026 real estate statistics have been published.

Fort Lauderdale Area Reports

Single Family Homes

Condominium & Townhouses

Fort Lauderdale Real Estate Market — February 2026

The February 2026 Fort Lauderdale real estate market shows contrasting trends between single-family homes and condos/townhomes, driven by declining inventory, shifting buyer behavior, and price stabilization.

Single-Family Homes

Inventory continues tightening, with new listings down 37.5% year-over-year (288 vs. 461). Despite fewer homes available, closed sales increased 5.7%, signaling strong buyer demand. Prices remained relatively stable:

- Median sold price: $722,500 (↓1.7%)

- Average sold price: $1.46M (↑2.87%)

- Median days on market: 51 (↓13.6%)

Sellers maintain an advantage in the mid‑to‑high‑end market, with a 94.9% list-to-sold ratio.

Condo / Townhome Market

The condo market also experienced a sharp decline in new listings (down 36.9%), but sales jumped 11.1% year-over-year, creating upward pressure in certain sub‑markets. Price activity was mixed:

- Median sold price: $477,687 (↓14.7%)

- Average sold price: $710,758 (↓6.3%)

- Days on market: 87 (↑31.8%)

While buyers have more negotiation power due to increasing DOM, the overall reduction in new listings indicates demand remains solid.

Market Snapshot

Across both segments, reduced inventory and consistent buyer activity are creating a competitive landscape, especially for well‑priced, turnkey properties. Luxury and waterfront listings in Fort Lauderdale continue to attract strong interest.

Commonly asked questions while reviewing the reports:

What is the difference between “Median Sales Price” and “Average Sales Price”?

Median Sales Price | Price of the “”middle”” property sold -an equal number of sales were above and below this price.

Average Sales Price | Average sales price for all properties sold.

What does “Absorption Rate” mean?

Absorption Rate | Looks at the past year’s monthly supply of inventory. In a normal market there should be a 6 month supply. The higher the rate above 6 the more aggressive a seller has to be with the competition; price and having a picture perfect property.

In this housing market in SE Florida, you need to work with an experienced and knowledgeable real estate professional. Please contact me if you would like to be sent updated market reports for YOUR specific neighborhood, Fort Lauderdale, or another SE Florida city. We can discuss the market, current trends and how we can work together to accomplish your real estate goals. I am here to help.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792

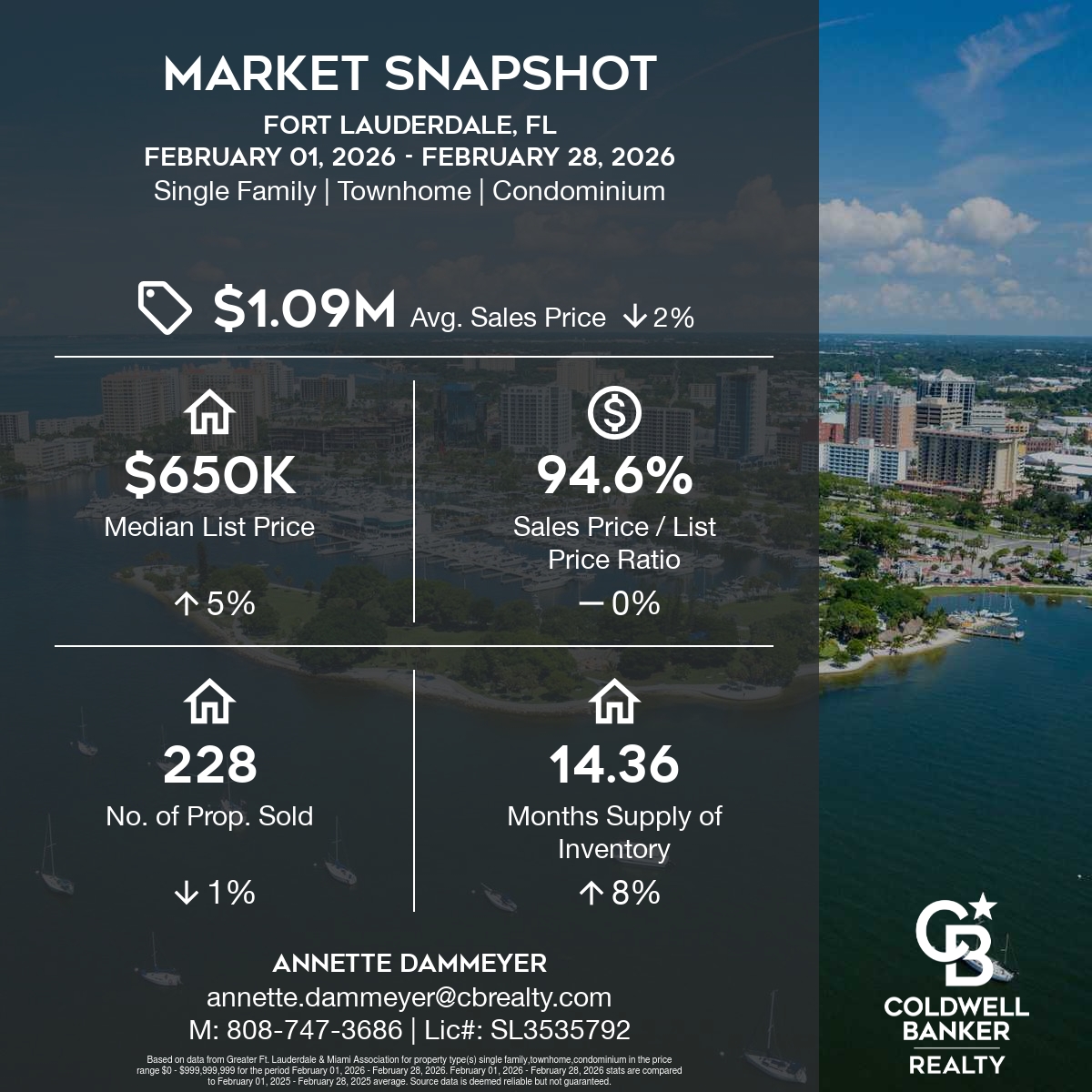

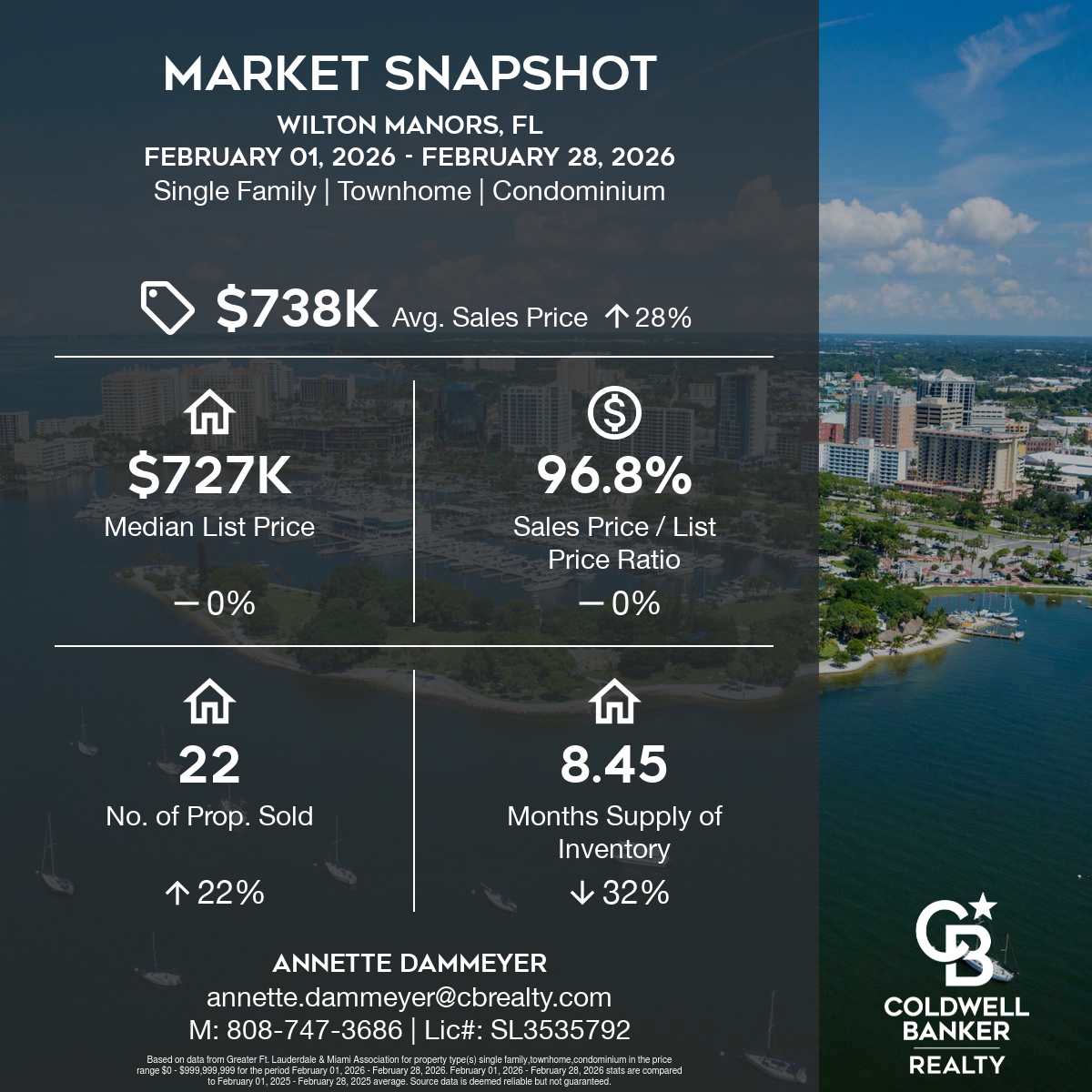

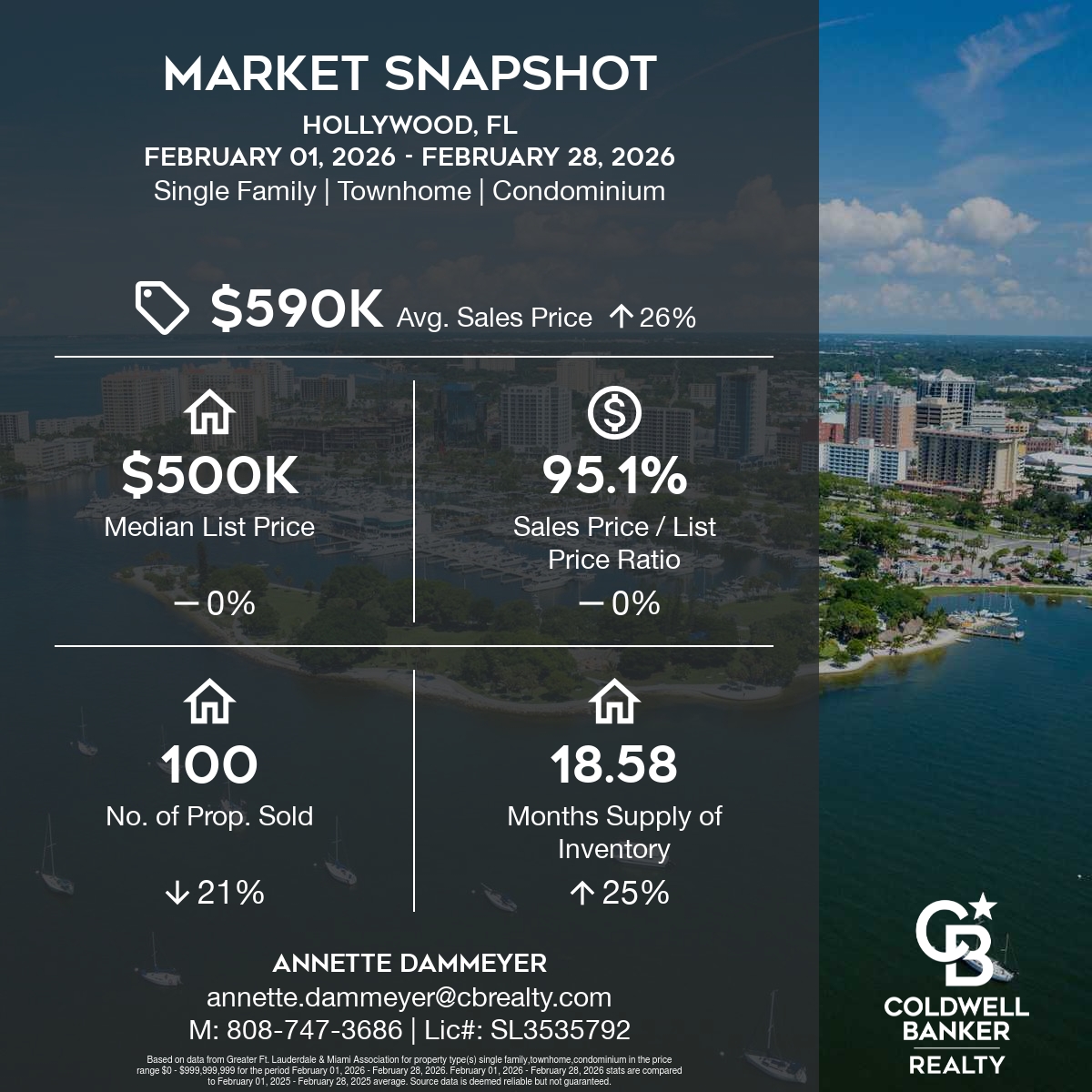

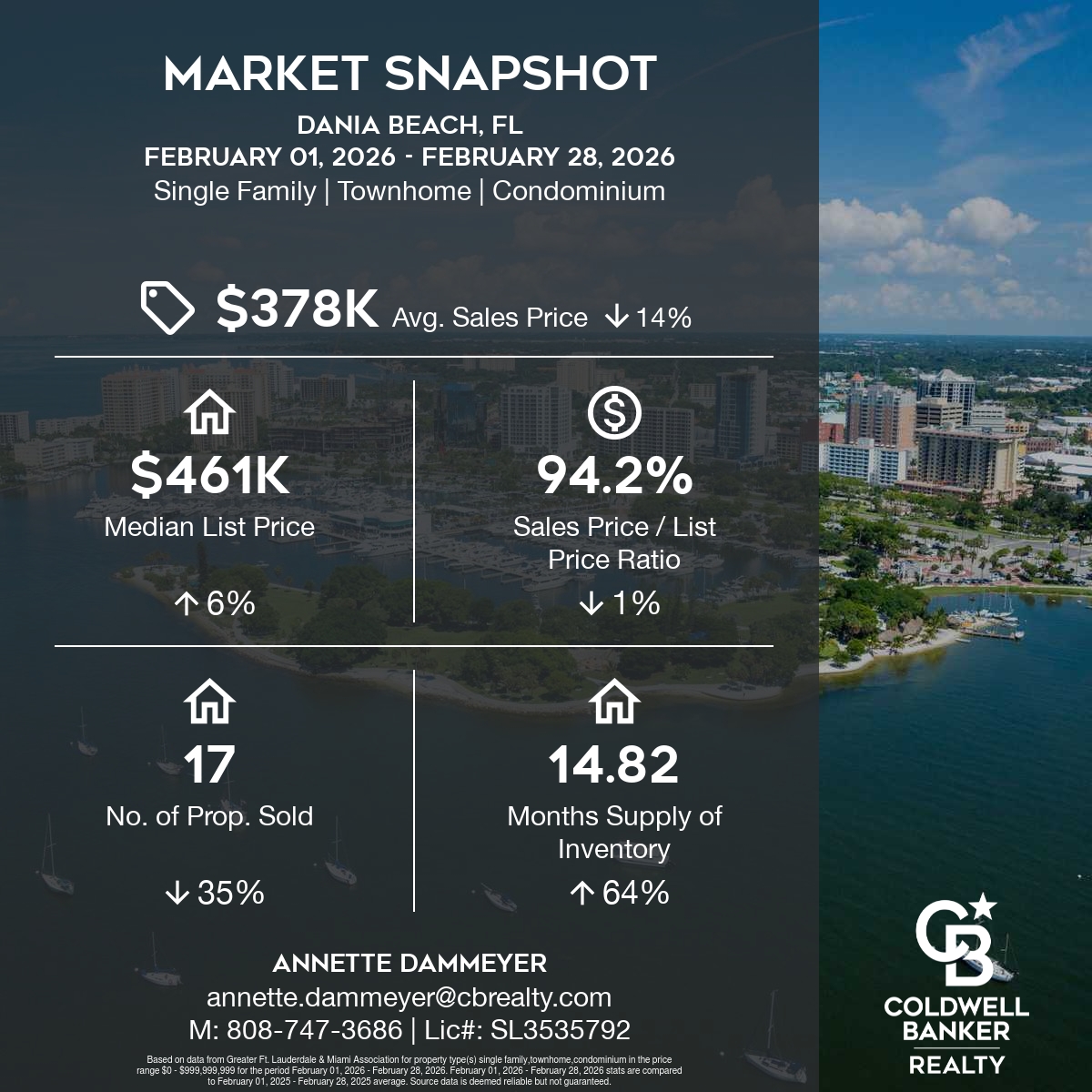

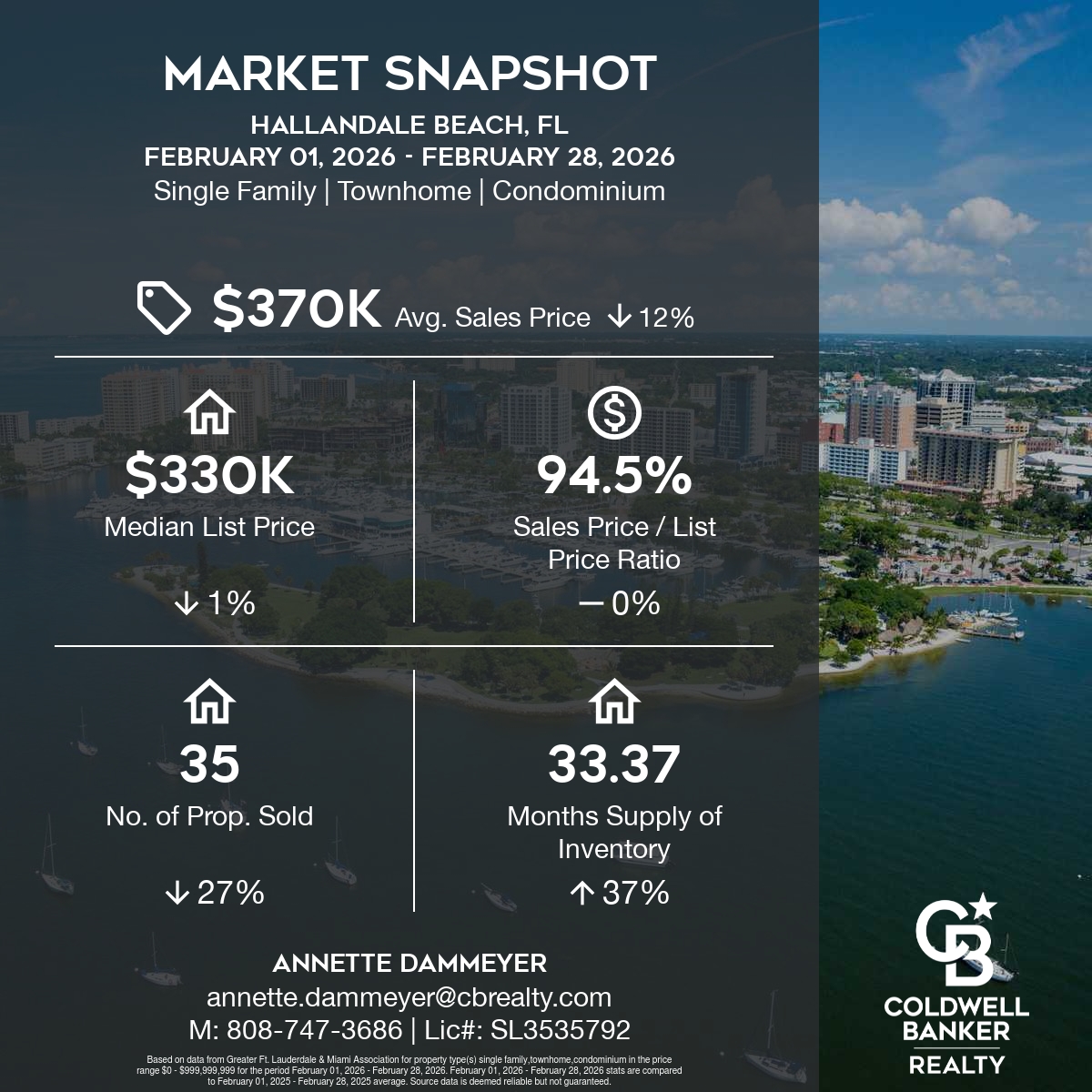

SE Florida Market Snapshot – February 2026

Market Trends in SE Florida

The real estate market is adjusting. With the fluctuation in property inventory, SE Florida is leaning towards a “buyer’s market”. Seller’s are now reassessing their asking price on their properties for sale. It is crucial to examine other similar homes on the market to establish an aggressive original listing price, generating multiple buyer’s attention to your property. This is also an important time to consider a decrease in asking price if the property has been on the market without active offers. I welcome any discussions you may want to have regarding your neighborhood trends. Please reach out to chat, even if you are not ready to buy or sell, but just would like to discuss current real estate updates. Here are the Market Snapshots reflecting the last month (compared to the same month last year) for the following areas:

- Fort Lauderdale

- Wilton Manors

- Hollywood

- Dania Beach

- Hallandale Beach

These take into account all property types (Single Family Homes/Condos/Townhomes).

The real estate landscape in South Florida is evolving. Making smart, timely decisions has never been more important. Whether you’re considering selling, buying, or simply staying informed, I’m here to be your local advisor and resource.

Let’s talk about current market trends and how we can align your goals with today’s opportunities. I’d be happy to provide customized market reports for Fort Lauderdale, any SE Florida city, or even your specific neighborhood—all automatically delivered to your inbox.

Call or email me anytime. I’m here to help you move forward with clarity and confidence.

CONTACT ANNETTE

Let’s start working together!

Annette Dammeyer, REALTOR®, ABR®, AHWD®

Coldwell Banker Realty

901 E Las Olas Blvd STE 101, Fort Lauderdale, FL 33301

808.747.3686

SL 3535792